FinTSBridge: A New Evaluation Suite for Real-World Financial Prediction with Advanced Time Series Models

https://arxiv.org/pdf/2503.06928

Abstract

Problem:

- 기존 TSF 모델들이 많이 발전했음에도

- Financial asset pricing에 실제로 적용하는 데에는 여전히 큰 간극이 존재

Goal:

- 최신 TSF 모델과 Finance 예측 문제를 연결하는 체계적인 evaluation bridge를 구축

Proposal: FinTSBridge

-

Dataset: 3개의 real-world financial TS dataset

-

Models: 10개 이상의 TSF 모델

-

Metrics

-

(기존) MSE, MAE

-

(제안) msIC, msIR

- Finance 예측에서 중요한 time series correlation을 평가하기 위해

-

1. Introduction

(1) Problem Setting

-

최근 TSF 모델은 크게 발전했으나, 이를 financial asset pricing에 실제로 적용하는 데에는 여전히 큰 간극이 존재

-

Limitations of Existing Benchmarks

- 기존 TS benchmark는 stationarity, periodicity가 강한 데이터(electricity, traffic)에 편중

- (1) Dataset 한계점: 기존 financial dataset은

- Daily resolution → intraday dynamics 소실

- Limited variables → derivatives, multi-scale interaction 미반영

- (2) Metric 한계점: MSE, MAE 중심 평가는

- Point-wise accuracy만 측정

- temporal correlation 및 market trend alignment를 반영하지 못함

- 단순 last-value predictor도 MSE는 양호하나 → 실제 trading 관점에서는 무의미함

(2) Motivation

Financial TS에서는

-

(1) 예측 정확도

-

(2) time-series correlation

-

(3) economic utility

를 함께 평가하는 framework가 필요

(3) Proposed Framework: FinTSBridge

최신 TS 모델과 real-world financial prediction을 연결하는 종합 evaluation suite

Key Components

- Financial-specific preprocessing

- stationarity를 강화하면서

- 변수 간 관계(inter-relationships)는 유지

- Modeling stage

- 다양한 AI-based TS forecasting 모델 적용

- Task design

- Multi-perspective forecasting tasks 설계

- Evaluation

- 기존 metric(MSE, MAE)

- 신규 metric(msIC, msIR)

- financial metric 기반 strategy simulation

(4) Goal

단순 예측 성능을 넘어, investment decision support 관점에서 TS 모델의 실질적 활용 가능성과 robustness를 평가

2. Related Works

(1) Financial Task-Related Studies

기존 Financial TS 예측 연구

- 주로 single-step forecasting

- Next-step price prediction

- Price movement (up/down) prediction

최근 연구 흐름

- Multi-horizon / multi-step forecasting으로 전환

- sequence-to-sequence models 활용

- 미래 여러 시점의 trajectory를 한 번에 예측

- exchange time series의 장기 temporal dynamics 포착 목적

Cutting-edge TS models와 financial tasks 사이의 bridge 필요성 제기!

(2) The Predictability of Asset Prices

Quantitative hedge funds

- Historical data에서 predictive signals을 지속적으로 발굴

- Changing market environment에서도 excess return 달성

Efficient Market Hypothesis (EMH)에 대한 재해석

- 일부 연구:

- 시장이 semi-strong 또는 strong-form efficiency를 항상 만족하지 않는다고 주장

- 실제 시장:

- weak-form과 semi-strong efficiency 사이에 위치하는 경우가 많음

- 경험적 근거

- Momentum effect

- 과거에 성과가 좋았던 자산이 미래에도 지속될 가능성

- Weak-form EMH에 대한 반례

- Multi-factor models

- asset pricing anomalies를 설명

- 시장 효율성이 제한적임을 간접적으로 시사

- Momentum effect

기술 발전의 영향

-

Data processing capability의 비약적 향상

-

과거에는 불가능했던

- Large-scale data

- Complex non-linear patterns

을 활용한 predictive models 등장

Summary

- Finance 시장은 완전 효율적이지 않으며

- 적절한 데이터, 모델, 평가 프레임워크 하에서는 asset price predictability가 실질적으로 존재!

3. Dataset Curation

기존 TS benchmark의 한계?

- Long-term TS forecasting 연구: Electricity, weather, traffic, exchange rate 중심의 8개 mainstream dataset에 집중

- Financial TS: Non-stationary, non-periodic 특성으로 인해 종종 제외되거나 ILI dataset으로 대체됨

그 결과: SOTA TS models는

- Controlled dataset에서는 성능이 높지만

- Real-world financial TS의 복잡성에 대한 robustness 부족

핵심 문제의식: 실제 Finance 문제를 반영하는

-

데이터 복잡성

-

비정상성

-

다양한 frequency

를 포함한 financial-specific dataset 필요!

(1) Data Sources

FinTSBridge는 3개의 Finance TS dataset을 구축

- 서로 다른 Finance sub-domain을 대표

a) GSMI

- Global stock market indices

- 20개 주요 지수

- daily frequency

- 기간: 2005–2024 (약 20년)

- 변수: price, trading volume

b) OPTION

- Chinese CSI 300ETF options

- call / put option의 risk-related variables

- derivative market 특성 반영

c) BTCF

- Bitcoin spot + perpetual futures

- hourly frequency

- spot–contract lag 분석

- long–short trading strategy 평가에 적합

Contribution

- Frequency, asset type, market structure가 다른 TS를 포괄

- 기존 benchmark 대비 현실 Finance 환경에 근접

(2) Data Preprocessing Methods

문제 배경: Finance TS는

- 변수 간 scale 차이가 큼

- 통일된 preprocessing 방식이 존재하지 않음

\(\rightarrow\) Task-specific preprocessing 필요

a) Log-return 기반 가격 변환 (GSMI, BTCF)

Notation

- Close price series 정의

- \(P^c_{0,t} = \{p^c_0, p^c_1, \dots, p^c_t\}\).

- Price change ratio

- \(R^c_i = \frac{p^c_i}{p^c_{i-1}}\).

- Log transformation

- \(\ln\left(\frac{P^c_{0,t}}{p^c_0}\right) = \{0, \ln(R^c_1), \dots, \ln(R^c_t)\}\).

의미

- Log price는 cumulative sum of log-returns

- 이전 시점 변화에만 의존 → additivity property

- Non-stationarity 완화

b) High price 변환 및 관계 유지

Notation

- High price series

- \(P^h_{0,t} = \{p^h_0, p^h_1, \dots, p^h_t\}\).

- Relative change to last close

- \(R^h_i = \frac{p^h_i}{p^c_{i-1}}\).

- Log transformation

- \(\ln\left(\frac{P^h_{0,t}}{p^c_0}\right) = \{0, \ln(R^h_1), \dots, \ln(R^h_t)\}\).

Close–high 관계

- \(\Delta(P^h, P^c) = \ln\left(\frac{P^h_{0,t}}{p^c_0}\right) - \ln\left(\frac{P^c_{0,t}}{p^c_0}\right) = \{\ln(\tfrac{R^h_i}{R^c_i})\}\).

장점

- OHLC 간 상대적 관계 보존

- 각 시점의 price structure 유지

c) Baseline anchoring

Notation

- 최종 가격 TS

- \(Z_{0,t} = \ln\left(\frac{P_{0,t}}{p^c_0}\right) + 100\).

- 목적

- Cumulative log 값의 음수 방지

- 모델 학습 안정성 향상

d) Trading volume

Notation

- Volume series

- \(V_{0,t} = \{v_0, v_1, \dots, v_t\}\).

- log transform

- \(Z^v_{0,t} = \ln(V_{0,t} + 1)\).

목적

- Zero volume로 인한 log 오류 방지

- scale 안정화

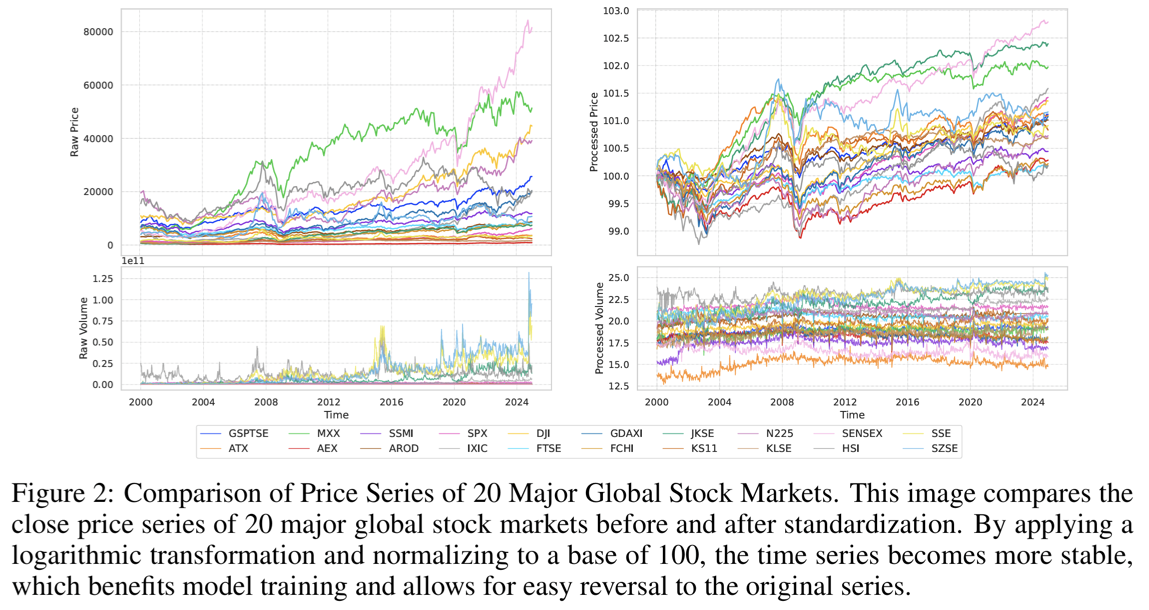

(3) Visualization of Preprocessing

목적: 제안한 preprocessing이

-

(1) scale 정렬

-

(2) 변수 간 상대적 구조 보존

을 실제 데이터에서 어떻게 달성하는지 시각적으로 검증

**[LEFT] Preprocessing 이전**

- Closing price

- 지수별 변동 폭과 절대 크기가 크게 다름

- Cross-sectional 비교가 어려움

- Trading volume

- Temporal fluctuation이 매우 불안정

- 지수 간 volume 비교가 거의 불가능

[Right] Preprocessing 이후

- Price & volume 모두

- 동일한 magnitude range로 정렬

- Price series는 공통 초기 baseline에 anchor

효과

- Cumulative change 비교 가능

- 지수 간, 변수 간 일관된 비교 가능성 확보

4. New Evaluation Metrics

(1) 문제의식

기존 TS forecasting 평가

- 주로 MSE, MAE 같은 error-based metric에 의존

Finance TS

- 단순한 Naive model (last value prediction)도 낮은 MSE 달성 가능

- 실제 시장 trend, correlation을 거의 포착하지 못함

결론

- Finance TS에서는 prediction error + correlation metric이 함께 필요

(2) 기존 Correlation metric의 한계

Information Coefficient (IC), Information Ratio (IR)

- single-step

- univariate

\(\rightarrow\) Multi-step, multivariate forecasting 성능을 평가하기에는 부적합

(3) Proposal

두 개의 metric 제안

- msIC (multi-step IC)

- msIR (multi-step IR)

목적: multi-step, multivariate TS 예측에서, 아래의 두 가지를 동시에 평가

- Temporal correlation

- Stability

a) msIC (Multi-step Information Coefficient)

Notation

- Input: \(X \in \mathbb{R}^{B \times L \times C}\)

- \(B\): batch size

- \(L\): input length

- \(C\): number of variables

- Prediction: \(\hat{Y} = f(X; \theta), \quad Y, \hat{Y} \in \mathbb{R}^{B \times F \times C}\)

- \(F\): forecast horizon

msIC 정의

- (각 sample \(i\), 변수 \(j\)에 대해) Prediction horizon F에 대한 rank correlation

- \(\rho_{Y_{i,j}, \hat{Y}_{i,j}} = \frac{\text{Cov}(Y_{i,j}, \hat{Y}_{i,j})} {\sigma_{Y_{i,j}} \, \sigma_{\hat{Y}_{i,j}}} \tag{14}\).

- msIC 계산

- \(\text{msIC} = \frac{1}{B \times C} \sum_{i=1}^{B} \sum_{j=1}^{C} \rho_{Y_{i,j}, \hat{Y}_{i,j}} \tag{15}\).

의미

- Multi-step TS 전반에서 true TS와 predicted TS 간 temporal correlation을 직접 측정

- (Error-based metric에서는 못잡아내는) trend consistency를 평가

b) msIR (Multi-step Information Ratio)

문제

- msIC는 평균 correlation만 측정

- sample 간 correlation stability는 반영하지 못함

msIR 정의

-

Sample-level msIC

- \(\text{msIC}_i = \frac{1}{C} \sum_{j=1}^{C} \rho_{Y_{i,j}, \hat{Y}_{i,j}} \tag{16}\).

-

msIC sequence

- \(\{\text{msIC}_1, \dots, \text{msIC}_B\}\).

- chronological order 유지

-

msIR 정의

-

\(\text{msIR} = \frac{\text{msIC}} {\sqrt{ \frac{1}{B} \sum_{i=1}^{B} (\text{msIC}_i - \text{msIC})^2 }} \tag{18}\).

- numerator

- 평균적인 effective correlation

- denominator

- correlation의 temporal variability (noise)

-

의미

- 높은 msIR

- 높은 correlation

- sample 간 안정적 성능

- 낮은 msIR

- 일부 구간만 잘 맞고

- 전반적 신뢰도 낮음

(4) Summary

- msIC는 “얼마나 잘 맞추는가”를 correlation 관점에서,

- msIR는 “그 성능이 얼마나 안정적인가”를 함께 평가하는 Finance TS 특화 metric

def msIC(Y, Y_hat):

B, F, C = Y.shape

rhos = []

for i in range(B):

for j in range(C):

y = Y[i, :, j]

y_hat = Y_hat[i, :, j]

rho = np.corrcoef(y, y_hat)[0, 1]

rhos.append(rho)

return np.mean(rhos)

def msIR(Y, Y_hat):

B, F, C = Y.shape

msic_per_sample = []

for i in range(B):

rhos = []

for j in range(C):

y = Y[i, :, j]

y_hat = Y_hat[i, :, j]

rhos.append(np.corrcoef(y, y_hat)[0, 1])

msic_per_sample.append(np.mean(rhos))

msic_per_sample = np.array(msic_per_sample)

return msic_per_sample.mean() / msic_per_sample.std()

5. Experiments

(1) M2M Forecasting

Setup

- Financial TS의 non-stationarity와 low signal-to-noise ratio를 고려한 실험 설계

- 3개 dataset × 16개 TS model 평가

- Forecasting horizon

- \(H \in \{5, 21, 63, 126\}\).

- Evaluation metrics

- Error-based: MSE, MAE

- Correlation-based: msIC, msIR

Results

- 모든 dataset·metric에서 절대적으로 우수한 단일 모델은 존재하지 않음

- [1] PSformer, TimeMixer, TiDE, PatchTST

- 대부분 task에서 안정적인 성능

- PSformer가 12개 중 8개 setting에서 최고 성능

- [2] Transformer, FEDformer

- Error metric에서는 열세

- 일부 dataset에서 correlation metric(msIC/msIR) 기준 경쟁력 존재

- [3] Naive model

- Predictive correlation은 거의 없음

- 그럼에도 MSE/MAE는 매우 낮아, 일부 SOTA 모델보다 우수

- Financial TS의 non-stationary 특성에서 흔히 관찰되는 현상

(2) M2U Forecasting

Setup

- 다변량 입력을 활용한 single target forecasting

- 단순 예측 성능 평가뿐 아니라

- Timing trading

- Long-short trading

- 등 실제 Finance application 기반 investment strategy 성능 평가 포함

Results

- Error metrics (MSE, MAE)

- Naive model이 대부분 경우에서 가장 낮은 loss

- PSformer, PatchTST, DLinear도 안정적인 성능

- GSMI, BTCF에서는 Naive가 최저 error

- Price TS의 예측 난이도와 직결

Correlation metrics (msIC, msIR)

- PSformer, Stationary, DLinear가 상대적으로 우수

-

PSformer는 12개 지표 중 9개에서 1–2위

- Strategy evaluation

- Figure 7: GSMI 시장 타이밍 성능 시각화

- Table 2: 전략 수익률 및 통계 지표 비교

- 단순 예측 성능을 넘어 financial usability 관점에서 모델 차이를 명확히 보여줌

(3) M2P Forecasting

Setup

- 전체 변수 중 일부 변수만 예측하는 현실적 scenario

- GSMI dataset에서

- 20개 글로벌 index의 closing price만 target으로 설정

- 예측 결과를 활용한 portfolio selection strategy

- 동시에 보유하는 index 개수 변화에 따른 backtest 수행

Results

- Error metrics

- Naive, PatchTST가 상대적으로 우수

- Correlation metrics

- PSformer, Informer가 더 강한 성능

- Portfolio backtest

- 어떤 모델도 모든 holding size에서 일관된 최고 수익률은 아님

- 대부분 모델이

- 20개 index 평균 수익률보다 높은 cumulative return 달성

- 보유 index 수가 줄어들수록 이 경향이 더 뚜렷

(4) Summary

-

Financial TS에서는 error metric만으로는 모델을 평가할 수 없음

-

Correlation-based metric(msIC, msIR)과 strategy-level evaluation이 필수

-

PSformer는 전반적으로 가장 일관된 강자

-

Naive model의 강한 error 성능은

→ Finance TS 평가의 함정을 명확히 보여주는 사례

6. Conclusion

-

Advanced TSF models & Practical financial applications 간의 간극을 연결

-

Specialized financial datasets를 구축

- global indices, derivatives, cryptocurrency markets를 포괄

-

New metric 제안

- msIC와 msIR

- Multi-step forecasting에서의 temporal correlation을 정량화함