VCformer: Variable Correlation Transformer with Inherent Lagged Correlation for Multivariate Time Series Forecasting

Contents

- Abstract

- Introduction

- Related Works

- Method

- Background

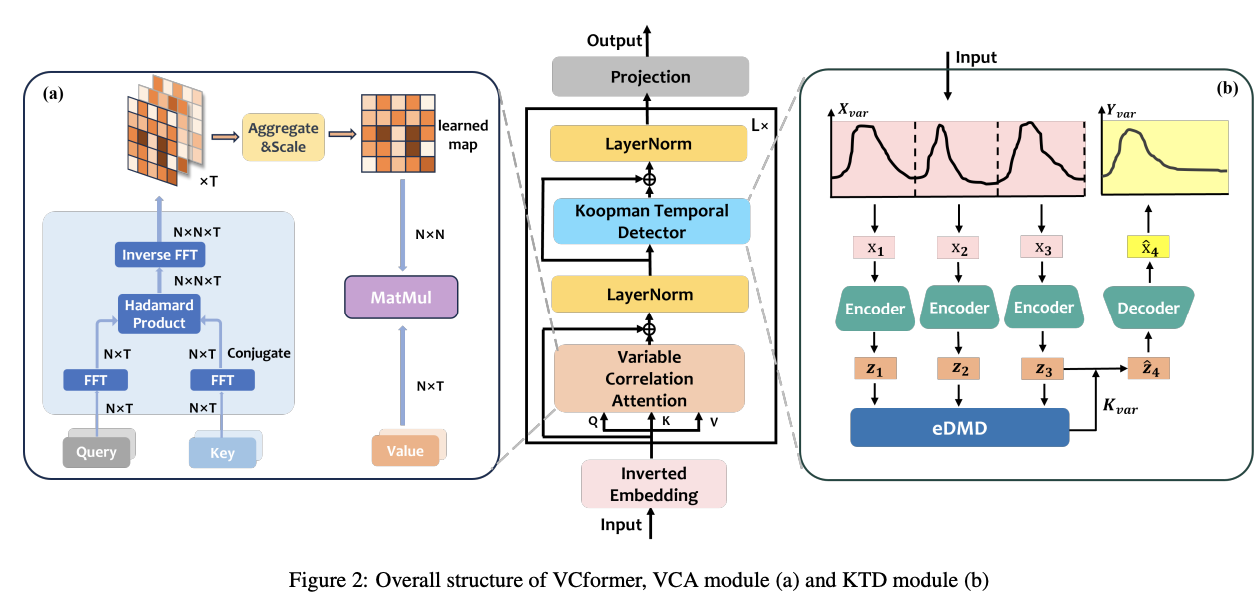

- Structure Overview

- Variable Correlation Attention

0. Abstract

Vanilla point-wise self-attention mechanism ?? NO!

Variable Correlation Transformer (VCformer)

- Utilizes Variable Correlation Attention (VCA) module

- to mine the correlations among variables

- VCA calculates and integrates the cross-correlation scores corresponding to different lags between queries and keys

- Koopman Temporal Detector (KTD)

- to better address the non-stationarity in TS

\(\rightarrow\) Extract both multivariate correlations and temporal dependencies

https://github.com/CSyyn/VCformer.

1. Introduction

Addressing the limitations of vanilla variable point-wise attention

Variable Correlation Transformer (VCformer)

-

Exploit lagged correlation inherent in MTS

- through the Variable Correlation Attention (VCA) module

-

VCA module

-

calculates the global strength of correlations between each query and key across different feature.

-

Not only computes autocorrelations akin to those in Autoformer

But also extends this concept to determine lagged crosscorrelations among various variates.

-

- ROLL operation + Hadamard products

- to approximate these lagged correlations effectively

- Adaptively aggregates lagged correlation over various lag lengths

- Koopman Temporal Detector (KTD) module

- inspired by Koopman theory in dynamics

Contributions

- VCformer

- Both variable correlations and temporal dependencies of MTS.

- Two things

- Fully exploit lagged correlations among different variates

- KD to effectively address non-stationarity

- SOTA

2. Related Works

CI vs. CD

pass

iTransformer [Liu et al., 2023a]

- revolutionizes the vanilla Transformer

- By inverting the duties of the

- (1) traditional attention mechanism

- (2) feed-forward network

- Roles

- (1) Capturing multivariate correlations

- (2) Learning nonlinear representations

- Adopt the classical self-attention mechanism based on point-wise method, which does not fully exploit the relationship among variable sequences.

3. Method

Input: \(\mathbf{X}=\) \(\left\{\mathbf{x}_1, \ldots, \mathbf{x}_T\right\} \in \mathbb{R}^{T \times N}\)

Target: \(\mathbf{Y}=\left\{\mathbf{x}_{T+1}, \ldots, \mathbf{x}_{T+H}\right\} \in\) \(\mathbb{R}^{H \times N}\)

(1) Background

- Limitation of vanilla variable attention

- in modelling feature-wise dependencies.

- Variable cross-correlation attention mechanism

- operates across the feature channels

- Koopman theory

- Treat TS as dynamics

- KTD module

- Combine it with the variable cross-correlation attention

- To learn both channels and time-steps dependencies

a) Limitation of Vanilla Variable Attnetion

Self-attention module

- employs the linear projections to get \(\mathbf{Q}, \mathbf{K}, \mathbf{V} \in \mathbb{R}^{T \times D}\),

- \(Q=\left[\mathbf{q}_1, \mathbf{q}_2, \ldots, \mathbf{q}_T\right]^{\top}\) ,

- \(K=\left[\mathbf{k}_1, \mathbf{k}_2, \ldots, \mathbf{k}_T\right]^{\top}\),

- Pre-Softmax attention score

- \(\mathbf{A}_{i, j}=\) \(\left(\mathbf{Q K}^{\top} / \sqrt{D}\right)_{i, j} \propto \mathbf{q}_i^{\top} \mathbf{k}_j\).

Nevertheless, feature-wise information,

( where each of the \(D\) features corresponds to an entry of \(\mathbf{q}_i \in \mathbb{R}^{1 \times D}\) or \(\mathbf{k}_j \in \mathbb{R}^{1 \times D}\) )

\(\rightarrow\) Absorbed into such inner-product representation :(

iTransformer [Liu et al., 2023a]

-

inverted Transformer, to capture cross-variable dependencies

- instead computes \(K^{\top} Q \in \mathbb{R}^{D \times D}\).

-

Suitable for capturing instantaneous cross-correlation,

but it is insufficient for MTS data which is coupled with the intrinsic temporal dependencies.

\(\rightarrow\) Variates of MTS data can be correlated with each other, yet with a lag interval!!

( = lagged cross-correlation in MTS analysis [John and Ferbinteanu, 2021; Chandereng and Gitter, 2020; Shen, 2015]. )

b) Non-linear Dynamics Tackled by Koopman Theory

Koopman theory [Koopman, 1931; Brunton et al., 2022]

-

linear dynamical system can be represented as an infinite-dimensional non-linear Koopman operator \(\mathcal{K}\)

-

which operates on a space of measurement functions \(g\), such that..

\(\mathcal{K} \circ g\left(x_t\right)=g\left(\mathbf{F}\left(x_t\right)\right)=g\left(x_{t+1}\right)\).

Dynamic Mode Decomposition(DMD) [Schmid and Sesterhenn, 2008]

- seeks the best fitted matrix \(K\) to approximate infinite-dimensional operator \(\mathcal{K}\) by collecting the observed system states

- Limitation: highly nontrivial to find appropriate measurement functions \(g\) as well as the Koopman operator \(\mathcal{K}\).

Koopman theory serves as a connection between ..

- finite-dimensional nonlinear dynamics

- infinite-dimensional linear dynamics

Proposal: KTD module (to tackle nonlinear dynamics)

- Consider TS data \(\mathbf{X}=\left\{\mathbf{x}_1, \ldots, \mathbf{x}_T\right\}\) as observations of a series of dynamic system states,

- where \(\mathbf{x}_i \in \mathbb{R}^N\) is the system state.

(2) Structure Overview

[1] Following the same Encoder-only structure as iTransformer

\(\rightarrow\) Adopt the Inverted Embedding : \(\mathbb{R}^T \mapsto \mathbb{R}^D\),

- which regards each UTS as the embedded token

[2] Stacking \(L\) layers with VCA and KTD modules

- [VCA] cross-variable relationships

- [KTD] temporal dependencies

[3] Final prediction (by the Projection) \(: \mathbb{R}^D \mapsto \mathbb{R}^H\).

(3) Variable Correlation Attention

a) Lagged Cross-correlation Computing

Stochastic process theory [Chatfield and Xing, 2019]

- Real discrete-time process \(\left\{\mathcal{X}_t\right\}\),

- Autocorrelation \(R_{\mathcal{X}, \mathcal{X}}(\tau)\)

- \(R_{\mathcal{X}, \mathcal{X}}(\tau)=\lim _{L \rightarrow \infty} \frac{1}{L} \sum_{\tau=1}^L \mathcal{X}_t \mathcal{X}_{t-\tau}\).

Approximation for the autocorrelation of variates \(i\) :

- \(R_{\mathbf{q}_i, \mathbf{k}_i}(\tau)=\sum_{\tau=1}^T\left(\mathbf{q}_i\right)_t \cdot\left(\mathbf{k}_i\right)_{t-\tau}=\mathbf{q}_i \odot \operatorname{ROLL}\left(\mathbf{k}_i, \tau\right)\).

- queries \(Q=\left[\mathbf{q}_1, \mathbf{q}_2, \ldots, \mathbf{q}_N\right]\)

- keys \(K=\) \(\left[\mathbf{k}_1, \mathbf{k}_2, \ldots, \mathbf{k}_N\right]\)

- where \(\mathbf{q}_i, \mathbf{k}_j \in \mathbb{R}^{T \times 1}\),

- \(\operatorname{ROLL}\left(\mathbf{k}_i, \tau\right)\): elements of \(\mathbf{k}_i\) shift along the time dimension

This idea was also harnessed in Autoformer [Wu et al., 2021].

Similarly, we can compute the cross-correlation between variate \(i\) and \(j\) by

- \(\text { LAGGED-COR }\left(\mathbf{q}_i, \mathbf{k}_j\right)=\mathbf{q}_i \odot \operatorname{ROLL}\left(\mathbf{k}_j, \tau\right)\).

b) Scores Aggregation

Total correlation of variate \(i\) and \(j\),

= Aggregate different lags \(\tau\) from 1 to \(T\)

( with learnable parameters \(\lambda=\) \(\left[\lambda_1, \lambda_2, \ldots, \lambda_T\right]\) )

- \(\operatorname{COR}\left(\mathbf{q}_i, \mathbf{k}_j\right)=\sum_{\tau=1}^T \lambda_i R_{\mathbf{q}_i, \mathbf{k}_j}(\tau)\).

VCA performs softmax on the learned multivariate correlation map \(\mathbf{A} \in \mathbb{R}^{N \times N}\) at each row and obtains the output via …

- \(\operatorname{VCA}(\mathbf{Q}, \mathbf{K}, \mathbf{V})=\operatorname{SOFTMAX}(\operatorname{COR}(\mathbf{Q}, \mathbf{K})) \mathbf{V}\).

(4) Koopman Temporal Detector (KTD)

Pass

(5) Efficient Computation

Pass