07. TS forecasting in TF

(참고) udemy - TF Developer in 2022

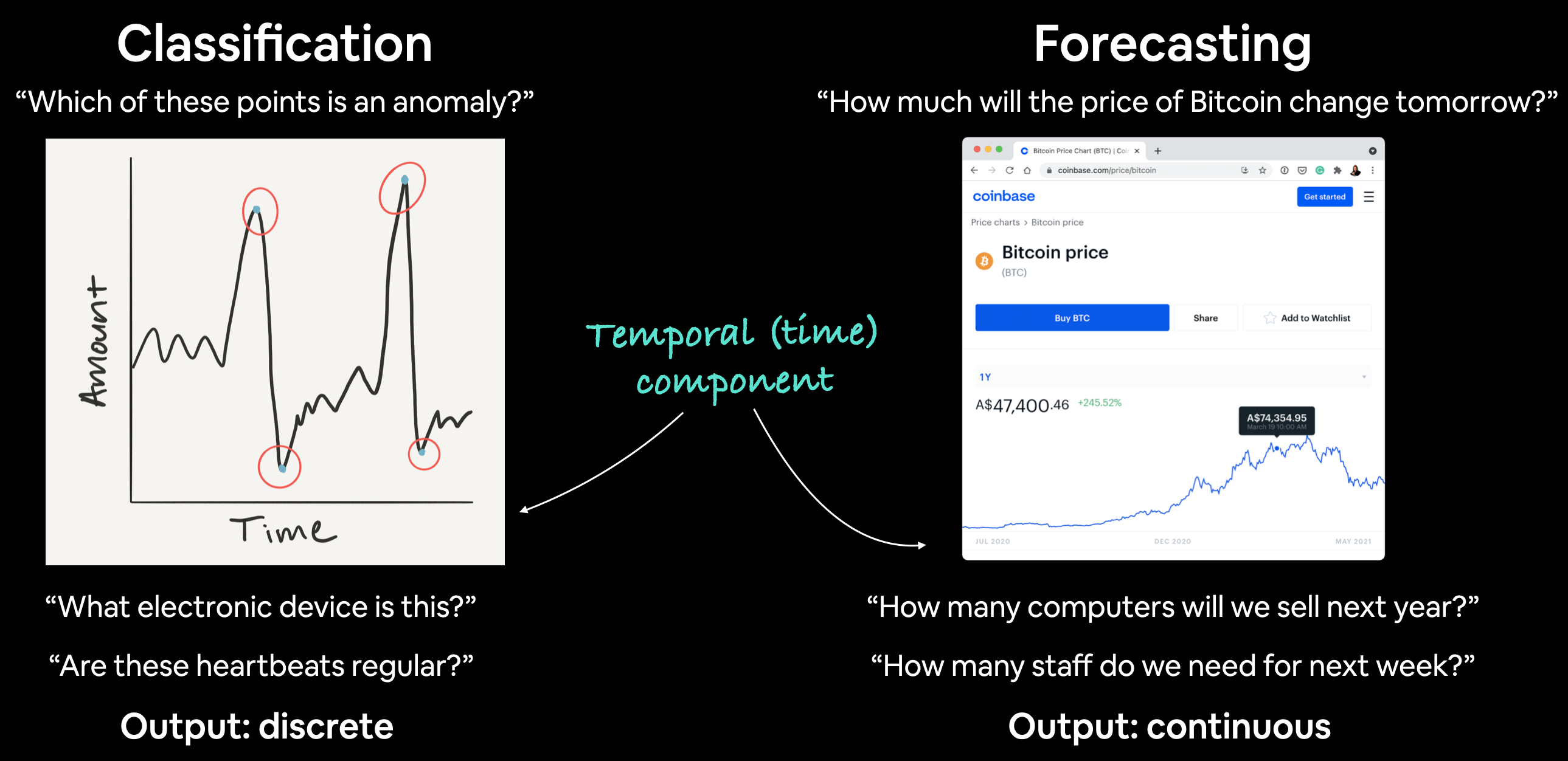

(1) TS forecasting & classification

| Examples | Output | |

|---|---|---|

| Classification | Anomaly detection, time series identification |

Discrete |

| Forecasting | Predicting stock market prices, forecasting future demand for a product, stocking inventory requirements |

Continuous |

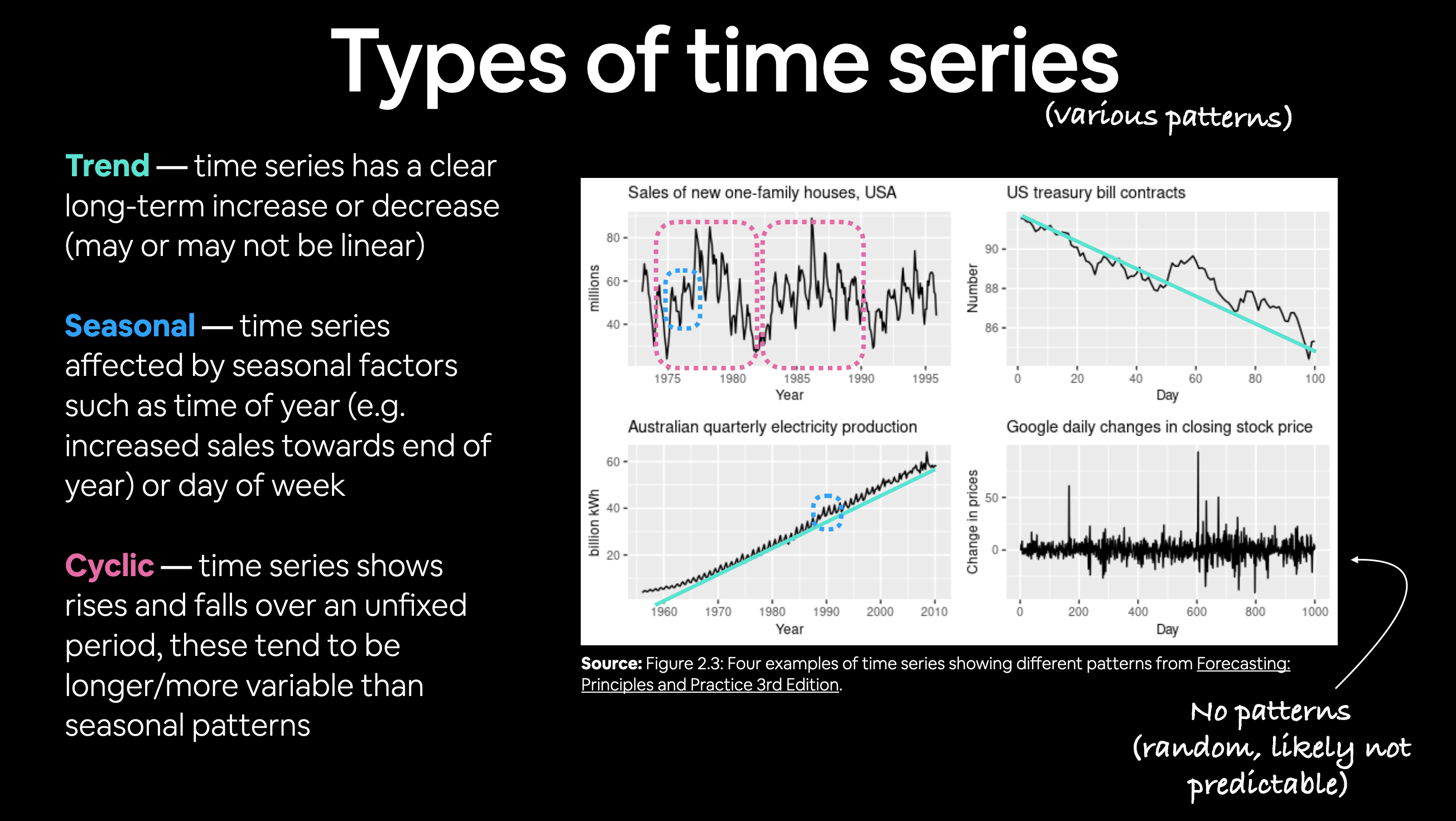

(2) Trend, Seasonality, Cycle

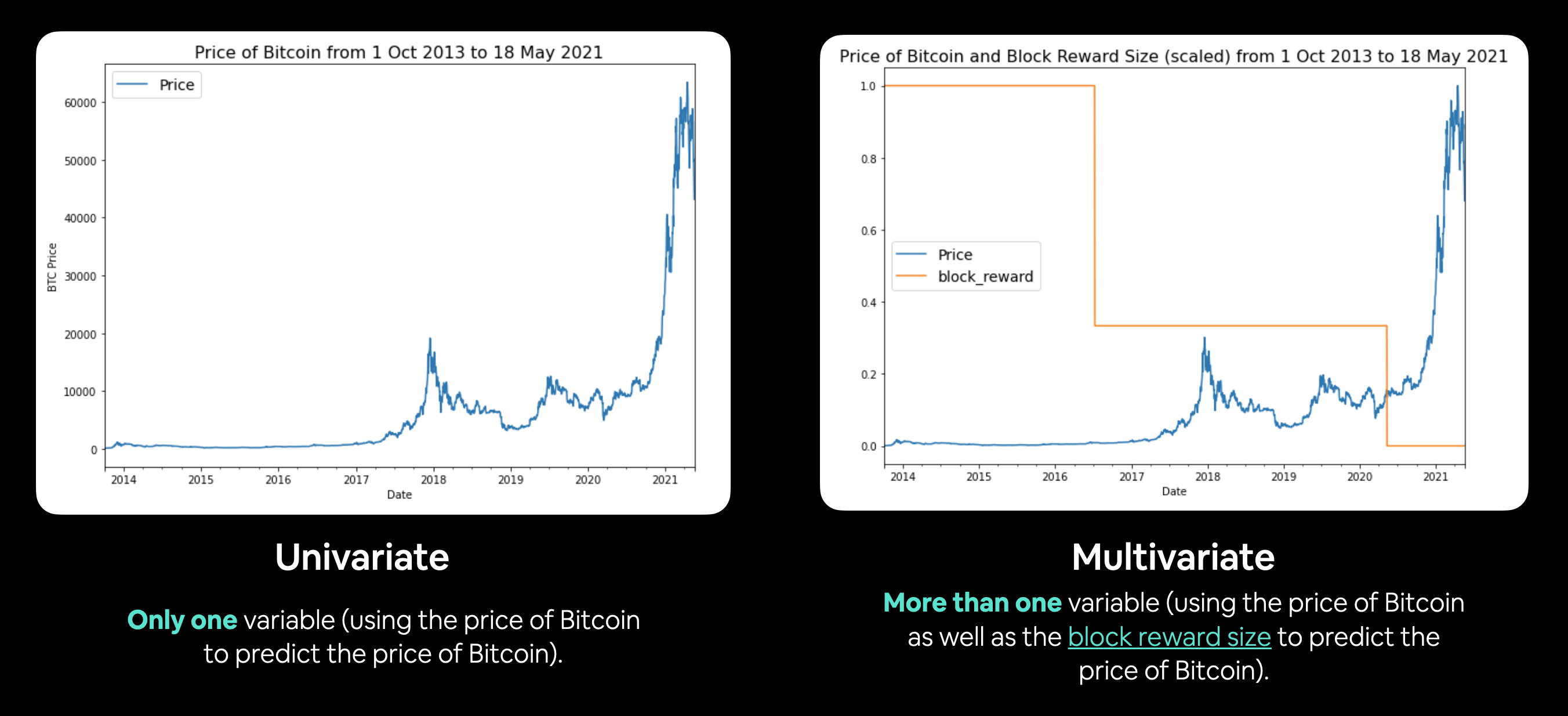

(3) Univariate vs Multivariate TS

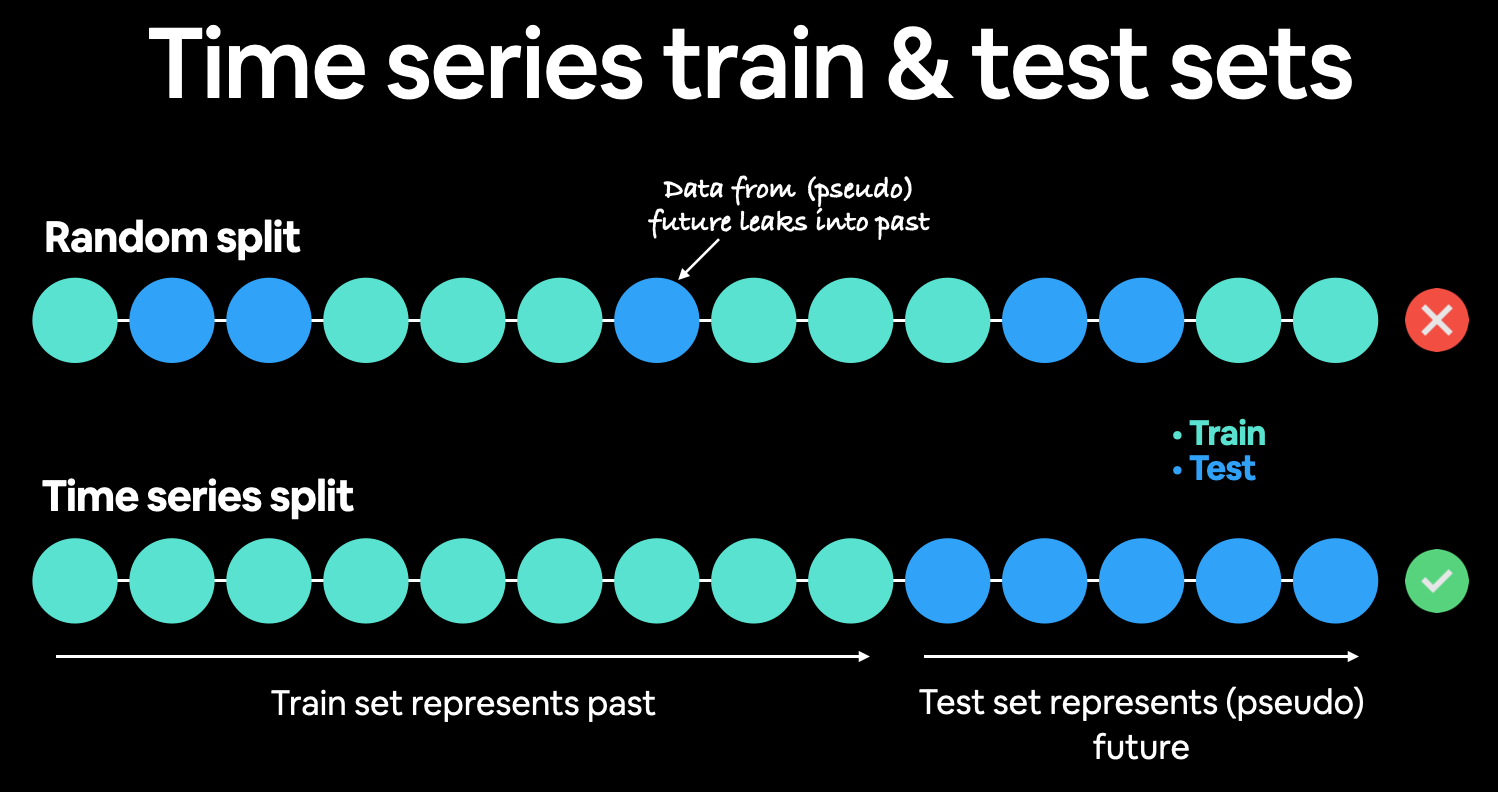

(4) Train & Test split in TS

split_size = int(0.8 * len(prices))

X_train, y_train = timesteps[:split_size], prices[:split_size]

X_test, y_test = timesteps[split_size:], prices[split_size:]

(5) Evaluating TS models

a) scale-dependent errors

b) percentage errors

- MAPE

tf.keras.metrics.mean_absolute_percentage_error()](https://www.tensorflow.org/api_docs/python/tf/keras/losses/MAPE)

- sMAPE

- Recommended not to be used by Forecasting: Principles and Practice, though it is used in forecasting competitions.

c) scaled errors

-

MASE

-

sktime’s

mase_loss() -

assuming no seasonality

def mean_absolute_scaled_error(y_true, y_pred): mae = tf.reduce_mean(tf.abs(y_true - y_pred)) mae_naive_no_season = tf.reduce_mean(tf.abs(y_true[1:] - y_true[:-1])) return mae / mae_naive_no_season -

(6) Baseline models

| Model/Library Name | Resource |

|---|---|

| Moving average | https://machinelearningmastery.com/moving-average-smoothing-for-time-series-forecasting-python/ |

| ARIMA (Autoregression Integrated Moving Average) | https://machinelearningmastery.com/arima-for-time-series-forecasting-with-python/ |

| sktime (Scikit-Learn for time series) | https://github.com/alan-turing-institute/sktime |

| TensorFlow Decision Forests (random forest, gradient boosting trees) | https://www.tensorflow.org/decision_forests |

| Facebook Kats (purpose-built forecasting and time series analysis library by Facebook) | https://github.com/facebookresearch/Kats |

| LinkedIn Greykite (flexible, intuitive and fast forecasts) | https://github.com/linkedin/greykite |

(7) Windowing Dataset

[0, 1, 2, 3, 4, 5, 6] -> [7]

[1, 2, 3, 4, 5, 6, 7] -> [8]

[2, 3, 4, 5, 6, 7, 8] -> [9]

(8) Checkpoint

import os

def create_model_checkpoint(model_name, save_path="model_experiments"):

return tf.keras.callbacks.ModelCheckpoint(filepath=os.path.join(save_path, model_name),

verbose=0,

save_best_only=True)

(9) model 0 : naive forecast

가장 마지막 값을 예측값으로

naive_forecast = y_test[:-1]

(10) model 1 : FC

Window = 7, Horizon = 1

HORIZON = 1

model_1 = tf.keras.Sequential([

layers.Dense(128, activation="relu"),

layers.Dense(HORIZON, activation="linear") ],

name="model_1_dense")

Window = 30, Horizon = 7

HORIZON = 7

model_2 = tf.keras.Sequential([

layers.Dense(128, activation="relu"),

layers.Dense(HORIZON) ],

name="model_2_dense")

(11) model 2 : Conv1D

- axis=1 (2번째 차원, channel 차원)에 1 넣어주기

model_4 = tf.keras.Sequential([

layers.Lambda(lambda x: tf.expand_dims(x, axis=1)),

layers.Conv1D(filters=128, kernel_size=5, padding="causal", activation="relu"),

layers.Dense(HORIZON)],

name="model_4_conv1D")

(12) model 3 : RNN (LSTM)

inputs = layers.Input(shape=(WINDOW_SIZE))

#------------------------------------------------------------------------------------#

x = layers.Lambda(lambda x: tf.expand_dims(x, axis=1))(inputs)

x = layers.LSTM(128, activation="relu")(x)

output = layers.Dense(HORIZON)(x)

#------------------------------------------------------------------------------------#

model_5 = tf.keras.Model(inputs=inputs, outputs=output, name="model_5_lstm")

(13) Ensembling results

def make_ensemble_preds(ensemble_models, data):

ensemble_preds = []

for model in ensemble_models:

preds = model.predict(data)

ensemble_preds.append(preds)

return tf.constant(tf.squeeze(ensemble_preds))

ensemble_preds = make_ensemble_preds(ensemble_models=ensemble_models,

data=test_dataset)

Prediction Interval

Prediction Intervals for Deep Learning Neural Networks

One way of getting the 95% condfidnece prediction intervals for a deep learning model is the bootstrap method:

- Take the predictions from a number of randomly initialized models

- Measure the standard deviation of the predictions

- Multiply standard deviation by 1.96

- (assuming the distribution is Gaussian, 95% of observations fall within 1.96 standard deviations of the mean, this is why we initialized our neural networks with a normal distribution)

- To get the prediction interval upper and lower bounds, add and subtract the value obtained in (3) to the mean/median of the predictions made in (1)

def get_upper_lower(preds):

preds_mean = tf.reduce_mean(preds, axis=0)

std = tf.math.reduce_std(preds, axis=0)

interval = 1.96 * std

lower, upper = preds_mean - interval, preds_mean + interval

return lower, upper

lower, upper = get_upper_lower(preds=ensemble_preds)

ensemble_median = np.median(ensemble_preds, axis=0)

offset=500

plt.figure(figsize=(10, 7))

plt.plot(X_test.index[offset:], y_test[offset:], "g", label="Test Data")

plt.plot(X_test.index[offset:], ensemble_median[offset:], "k-", label="Ensemble Median")

plt.xlabel("Date")

plt.ylabel("BTC Price")

plt.fill_between(X_test.index[offset:],

(lower)[offset:],

(upper)[offset:], label="Prediction Intervals")

plt.legend(loc="upper left", fontsize=14)