Dish-TS: A General Paradigim for Alleviating Distribution for Time Series Forecasting (AAAI 2023)

https://arxiv.org/pdf/2302.14829.pdf

https://github.com/weifantt/Dish-TS.

Contents

- Abstract

- Introduction

- 2 limitations of previous works

- Dish_TS

- Related Work

- Models for TSF

- Distribution Shift in TSF

- Problem Formulations

- TSF

- Distribution Shift in TS

- Dish-TS

- Overview

- Dual-Conet Framework

- A Simple and Intuitive Instance of Conet

- Experiment

- Experimental Setup

- Overall Performance

- Comparison with Normalization Methods

- Parameters and Model Analysis

Abstract

Problems of existing works towards distribution shift

- mostly limited in the quantification of distribution

- overlook the potential shift between lookback & horizon windows

Distribution shift in TSF into 2 categories

- INTRA-space shift : input space

- INTER-space shift : input space & outpt space

Dish-TS

-

general neural paradigm for alleviating distribution shift in TSF

-

propose the coefficient net (CONET)

-

as a Dual-CONET framework

-

\(\rightarrow\) to separately learn the distribution of input- and output-space

( = captures the distribution difference of two spaces 0

-

1. Introduction

(1) 2 limitations of previous works

- Distribution quantification for intra-space in TSF is unreliable

- the empirical statistics are unreliable & limited in expressiveness for representing the true distribution behind the data

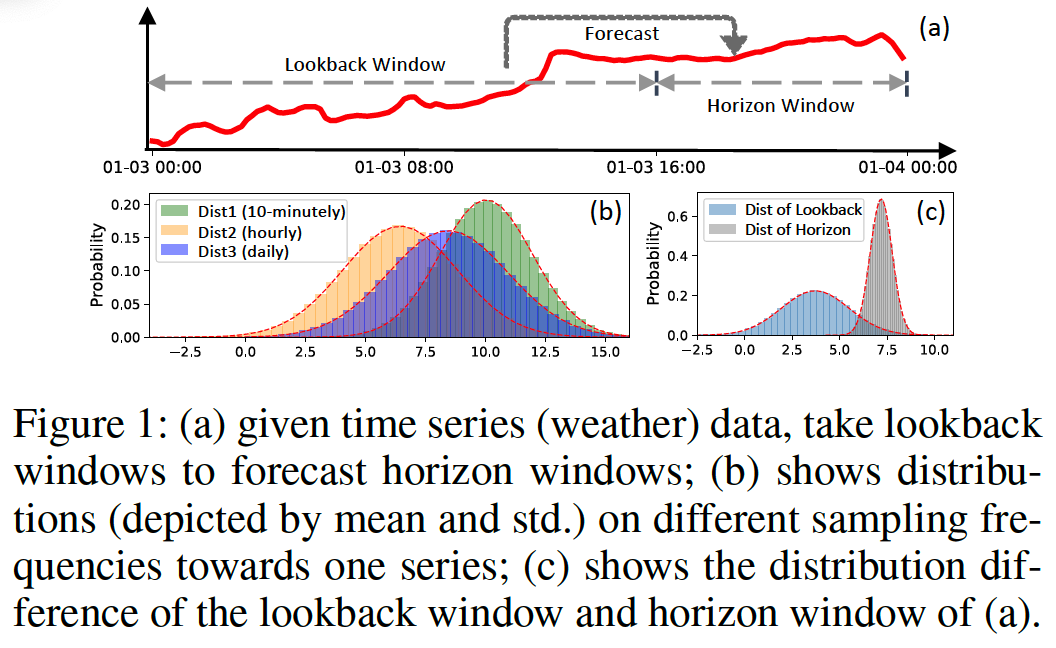

- ex) differ by sampling frequency ( fig 1(b) )

- Inter-space shift of TSF is neglected

- (preivous works) assume the input-space and output-space follow the same distribution

- RevIN??

- still limitation … strong assumption that the lookbacks and horizons share the same statistical properties ( = same distn )

- ex) ( fig 1(c) )

(2) Dish-TS

Dish-TS ( Distribution shift in Time Series )

- model-agnostic

- inspired by RevIN ( normalize & denormalize )

Problem 1) unreliable distribution quantification

Solution 1) coefficient net (CONET)

-

to measure the series distribution.

- given any window of series data, maps it into two learnable coefficients

- (1) level coefficient

- (2) scaling coefficient

- can be designed as any NN

Problem 2) intra-space shift & inter-space shift

Solution 2) as a DUAL-CONET

- consists of 2 separate CONETS

- (1) BackCONET

- coef for INPUT-space ( = lookbacks )

- (2) HoriCONET

- Chef for OUTPUT-space ( = horizons )

- (1) BackCONET

-

distinct distributions for input- and output-space

\(\rightarrow\) relieves the inter-space shift

2. Related Work

(1) Models for TSF

- pass

(2) Distribution Shift in TSF

Realworld series is changing over time (Akay and Atak 2007)

Adaptive Norm (Ogasawara et al. 2010)

- puts z-score normalization on series by the computed global statistics.

DAIN (Passalis et al. 2019)

- applies NN to adaptively normalize the series.

Adaptive RNNs (Du et al. 2021)

RevIN (Kim et al. 2022)

- instance normalization

Problem 1. ( Except for DAIN .. ) most works still used static statistics or distance function

\(\rightarrow\) limited in expressiveness.

Problem 2. Hardly consider the inter-space shift

- between model input-space and output-space.

3. Problem Formulations

(1) TSF

Notation

- \(x_t\) : value at time-step \(t\)

- input : \(\boldsymbol{x}_{t-L: t}=\left[x_{t-L+1}, \cdots, x_t\right]\)

- output : \(\boldsymbol{x}_{t: t+H}=\left[x_{t+1}, \cdots, x_{t+H}\right]\)

- \(L\) : the length of lookback windows

- \(H\) : the length of horizon windows

- \(N\) multivariate time series : \(\left\{x_t^{(1)}, x_t^{(2)}, \cdots, x_t^{(N)}\right\}_{t=1}^T\)

- MTSF task : \(\left(\boldsymbol{x}_{t: t+H}^{(1)}, \cdots, \boldsymbol{x}_{t: t+H}^{(N)}\right)^T=\mathscr{F}_{\Theta}\left(\left(\boldsymbol{x}_{t-L: t}^{(1)}, \cdots, \boldsymbol{x}_{t-L: t}^{(N)}\right)^T\right)\)

- mapping function \(\mathscr{F}_{\Theta}: \mathbb{R}^{L \times N} \rightarrow \mathbb{R}^{H \times N}\)

(2) Distn shift in TS

a) Intra-space shift

- for any time-step \(u \neq v\), \(\mid d\left(\mathcal{X}_{\text {input }}^{(i)}(u), \mathcal{X}_{\text {input }}^{(i)}(v)\right) \mid >\delta\)

- \(\delta\) is a small threshold

- \(d\) is a distance function (e.g., KL divergence)

- \(\mathcal{X}_{\text {input }}^{(i)}(u)\) and \(\mathcal{X}_{\text {input }}^{(i)}(v)\) : distributions

Most existing works:

- mention distribution shift in series, they mean our called intra-space shift

b) Inter-space shift

- \(\mid d\left(\mathcal{X}_{\text {input }}^{(i)}(u), \mathcal{X}_{\text {output }}^{(i)}(u)\right) \mid >\delta\).

( mostly ignored by current TSF models )

4. Dish-TS

(1) Overview

Dual CONET

- transform INPUT

- via coef obtained from BACKCONET

- transform OUTPUT

- via coef obtained from HORICONET

- becomes the forecasting output

(2) Dual-Conet Framework

illustrate how forecasting models are integrated into DualCONET

- by a two-stage normalize-denormalize process.

a) Conet (coefficient net )

\(\boldsymbol{\varphi}, \boldsymbol{\xi}=\operatorname{CONeT}(\boldsymbol{x})\).

- \(\varphi \in \mathbb{R}^1\) : level coefficient

- overall scale of input series in a window \(\boldsymbol{x} \in \mathbb{R}^L\)

- \(\boldsymbol{\xi} \in \mathbb{R}^1\) : scaling coefficient

- fluctuation scale of \(\boldsymbol{x}\).

b) Dual-Conet

Goal: to deal with intra-space shift and inter-space shift

\(\begin{aligned} & \boldsymbol{\varphi}_{b, t}^{(i)}, \boldsymbol{\xi}_{b, t}^{(i)}=\operatorname{BACKCONET}\left(\boldsymbol{x}_{t-L: t}^{(i)}\right), i=1, \cdots, N \\ & \boldsymbol{\varphi}_{h, t}^{(i)}, \boldsymbol{\xi}_{h, t}^{(i)}=\operatorname{HoRiCONET}\left(\boldsymbol{x}_{t-L: t}^{(i)}\right), i=1, \cdots, N \end{aligned}\),

- \(\boldsymbol{\varphi}_{b, t}^{(i)}, \boldsymbol{\xi}_{b, t}^{(i)} \in \mathbb{R}^1\) : coefficients for lookbacks

- \(\boldsymbol{\varphi}_{h, t}^{(i)}, \boldsymbol{\xi}_{h, t}^{(i)} \in \mathbb{R}^1\) : coefficients for horizons

\(\rightarrow\) share the same input \(\boldsymbol{x}_{t-L: t}^{(i)}\),

BACKCONET

- aims to approximate distribution \(\mathcal{X}_{\text {input }}^{(i)}\)

HORICONET

- aims to infer (or predict) future distribution \(\mathcal{X}_{\text {output }}^{(i)}\)

c) Integrating Dual-Conet into Forecasting

After acquiring coefficients from Dual-CONET…

\(\rightarrow\) the coefficients can be integrated into any TS

- through a two-stage normalizing-denormalizing process

original forecasting process \(\hat{\boldsymbol{x}}_{t: t+H}^{(i)}=\mathscr{F}_{\Theta}\left(\boldsymbol{x}_{t-L: t}^{(i)}\right)\) is rewritten as:

- \(\hat{\boldsymbol{x}}_{t: t+H}^{(i)}=\boldsymbol{\xi}_{h, t}^{(i)} \mathscr{F}_{\Theta}\left(\frac{1}{\boldsymbol{\xi}_{b, t}^{(i)}}\left(\boldsymbol{x}_{t-L: t}^{(i)}-\boldsymbol{\varphi}_{b, t}^{(i)}\right)\right)+\boldsymbol{\varphi}_{h, t}^{(i)}\).

(3) A Simple and Intuitive Instance of Conet

Flexibility of Dish-TS comes from the specific CONET design

- which could be any neural architectures for different modeling capacity.

Most intuitive way : FC layer

- Input : multivariate input \(\left\{\boldsymbol{x}_{t-L: t}^{(i)}\right\}_{i=1}^N\),

- FC layer : \(\mathbf{v}_b^{\ell}, \mathbf{v}_h^{\ell} \in \mathbb{R}^{L * N}\)

- ( consider \(\ell=1\) for simplicity )

- \(\boldsymbol{\varphi}_{b, t}^{(i)}=\sigma\left(\sum_{\tau=1}^{\operatorname{dim}\left(\mathbf{v}_{b, i}^{\ell}\right)} \mathbf{v}_{b, i \tau}^{\ell} x_{\tau-L+t}^{(i)}\right)\).

- \(\varphi_{h, t}^{(i)}=\sigma\left(\sum_{\tau=1}^{\operatorname{dim}\left(\mathbf{v}_{h, i}^{\ell}\right)} \mathbf{v}_{h, i \tau}^{\ell} x_{\tau-L+t}^{(i)}\right)\).

- \(\sigma\) : leaky ReLU

Scaling coefficients:

-

\(\boldsymbol{\xi}_{b, t}^{(i)}=\sqrt{\mathbb{E}\left(x_t^{(i)}-\boldsymbol{\varphi}_{b, t}^{(i)}\right)^2}\).

-

\(\boldsymbol{\xi}_{h, t}^{(i)}=\sqrt{\mathbb{E}\left(x_t^{(i)}-\varphi_{h, t}^{(i)}\right)^2}\).

- can be seen as the average deviation of \(\boldsymbol{x}_{t-L: t}^{(i)}\) with regard to \(\boldsymbol{\varphi}_{b, t}^{(i)}\) and \(\boldsymbol{\varphi}_{h, t}^{(i)}\).

5. Experiment

(1) Experimental Setup

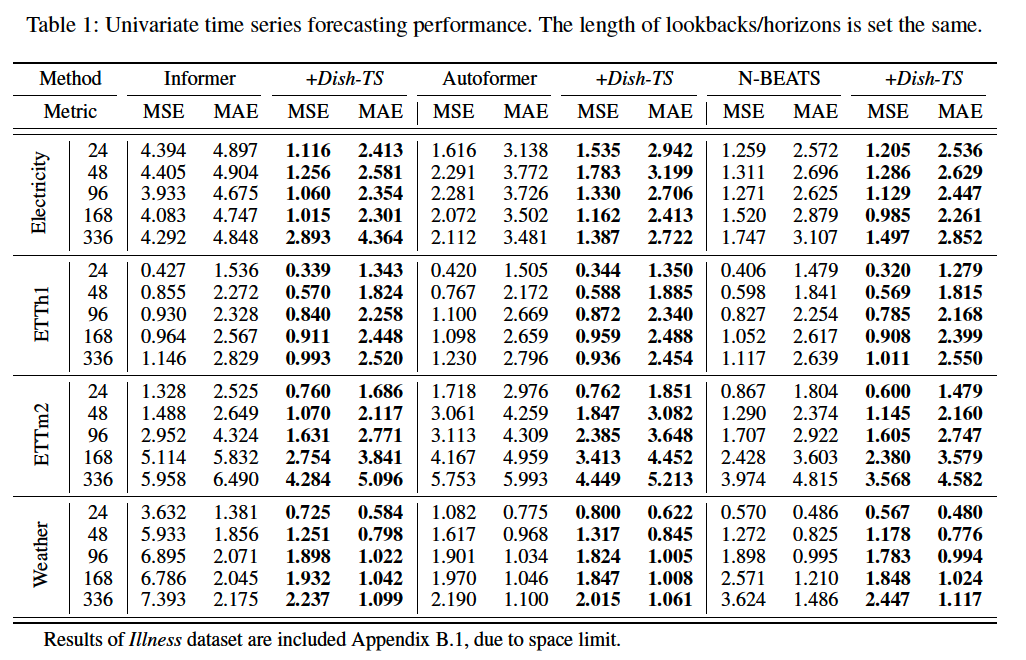

a) Dataset

- Electricity

- ETT (ETTh1, ETTm2)

- Weather

- Illness

b) Evaluation

without data normalization or scaling

-

evaluations are on original data

\(\rightarrow\) thus the reported metrics are scaled for readability.

c) Implementation

- lookback length = horizon length

- except for Illness) from 24 to 336

d) Baselines

3 SOTA models

- Informer

- Autoformer

- N-Beats

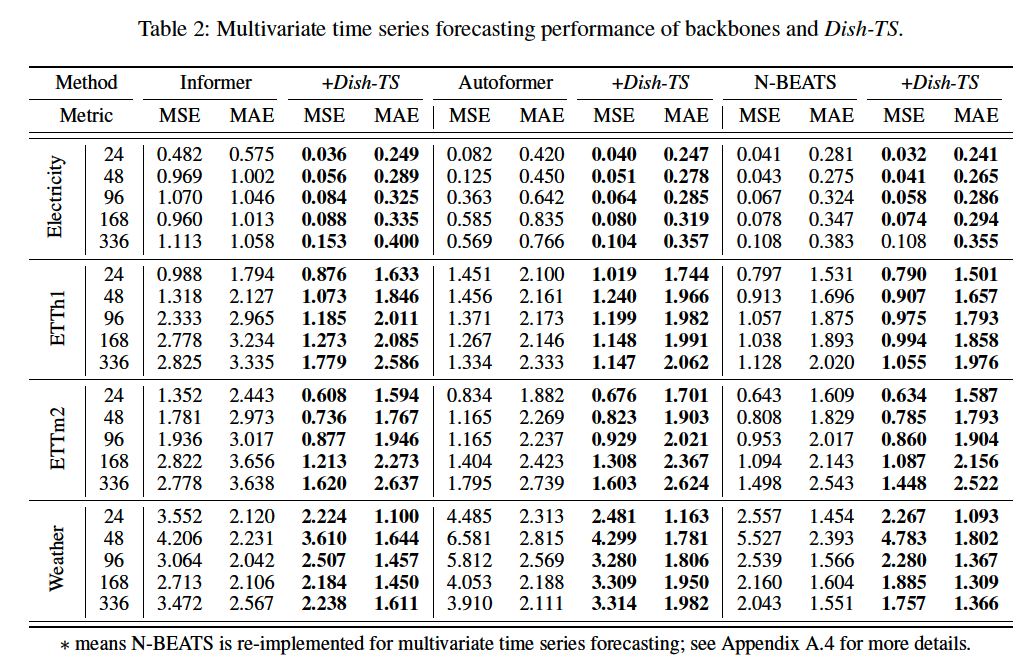

(2) Overall Performance

a) UTS forecasting

b) MTS forecasting

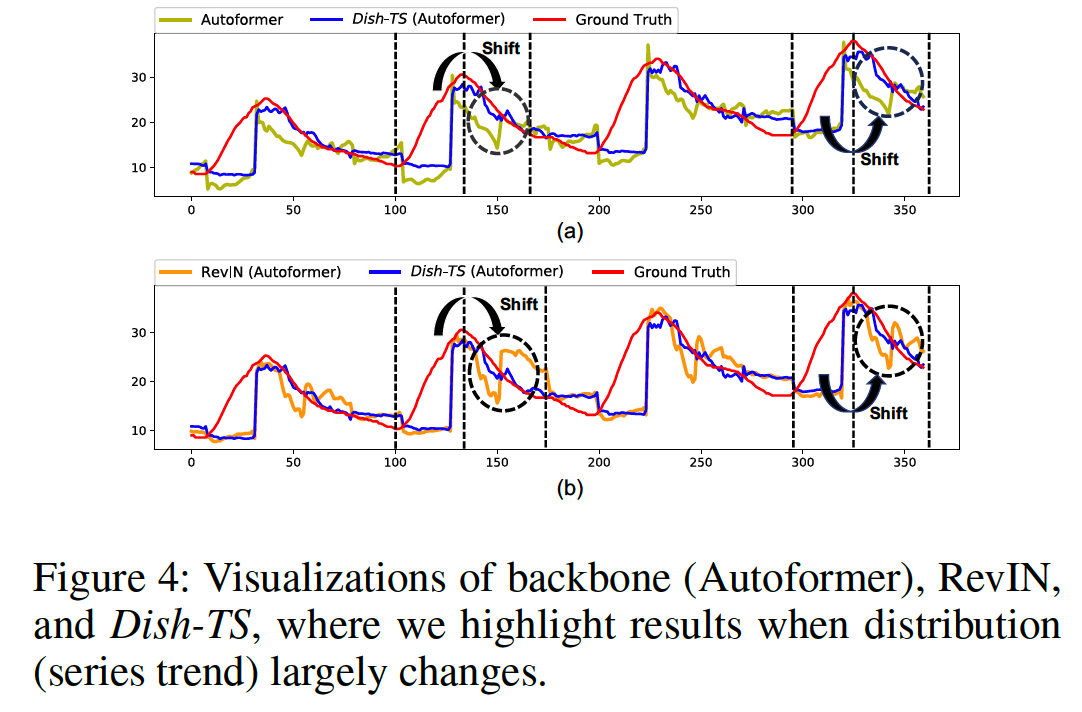

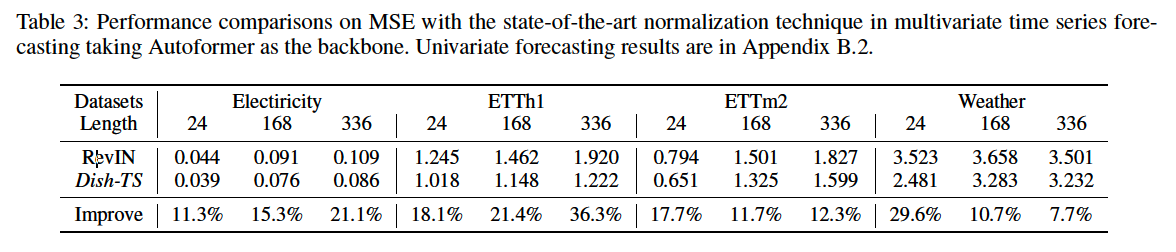

(3) Comparison with Normalization Methods

compare with RevIN (Kim et al. 2022)

( don’t consider AdaRNN (Du et al. 2021), because it is not compatible for fair comparisons )

A potential reason ?

\(\rightarrow\) consideration towards both intra-space shift and inter-space shift.

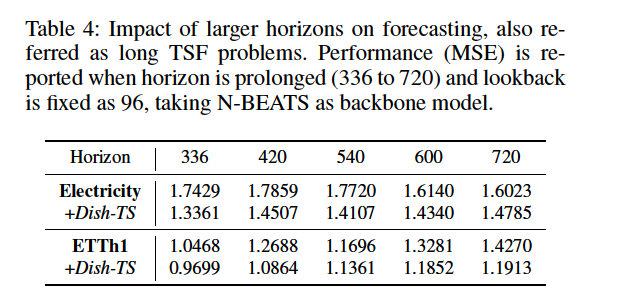

(4) Parameters and Model Analysis

a) Horizon (\(H\)) Analysis

Effect of using larger horizons ( = LTSF )

- fix \(L = 96\)

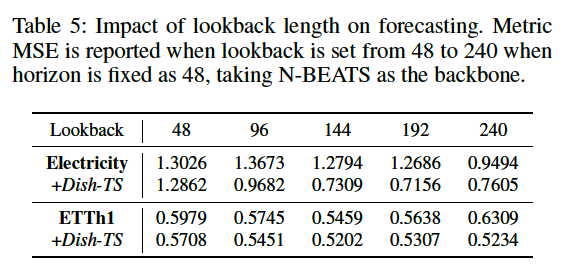

b) Lookback (\(L\)) Analysis

Effect of using larger input length

- fix \(H = 48\)

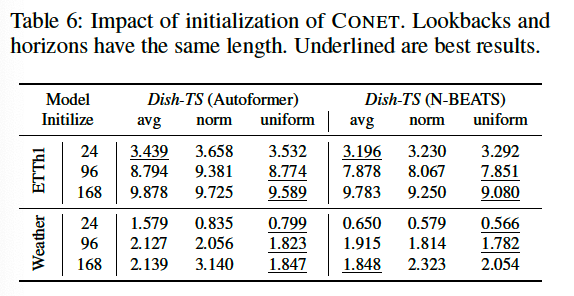

c) Conet Initialization

Initialization for FC layer : \(\mathbf{v}_b^{\ell}, \mathbf{v}_h^{\ell} \in \mathbb{R}^{L * N}\)

avg: 1norm: \(N(0,1)\)uniform: \(U(0,1)\)

Result: do not use norm !

d) Visualizations