Neural Basis Expansion analysis with exogenous variables ; Forecasting electricity prices with NBEATSx (2021)

Contents

- Abstract

- Introduction

- Literature Review

- DL & Sequence Modeling

- Electricity Price Forecasting (EPF)

- NBEATSx Model

- Stacks and Blocks

- Residual Connections

0. Abstract

neural basis expansion analysis (NBEATS) to incorporate exogenous factors

- extend its capabilities by including “exogenous variables”

1. Introduction

DL for forecasting tasks … example )

- ESRNN (Exponential Smoothing Recurrent Neural Network)

- NBEATS (Neural Basis Expansion Analysis)

Still, 2 possible improvements!

- 1) integration of time-dependent exogenous variables

- 2) interpretability of NN outputs

2. Literature Review

(1) DL & Sequence Modeling

a) basic models

- RNN, LSTM, GRU

b) adoptions of Conv & Skip-connection within RNN

- WaveNet

- Dilated RNN (DRNN)

- Temporal Convolutional Network (TCN)

c) Seq2Seq

- better forecasting performance than classical statistical methods

(2) Electricity Price Forecasting (EPF)

EPF task : predicting the spot & forward prices in the market

- mostly focus on predicting “24 hours of the next day”

- either at “point” or “probabilistic” setting

- majority of NN solving EPF suffer…

- too short/limited to ONE market test period

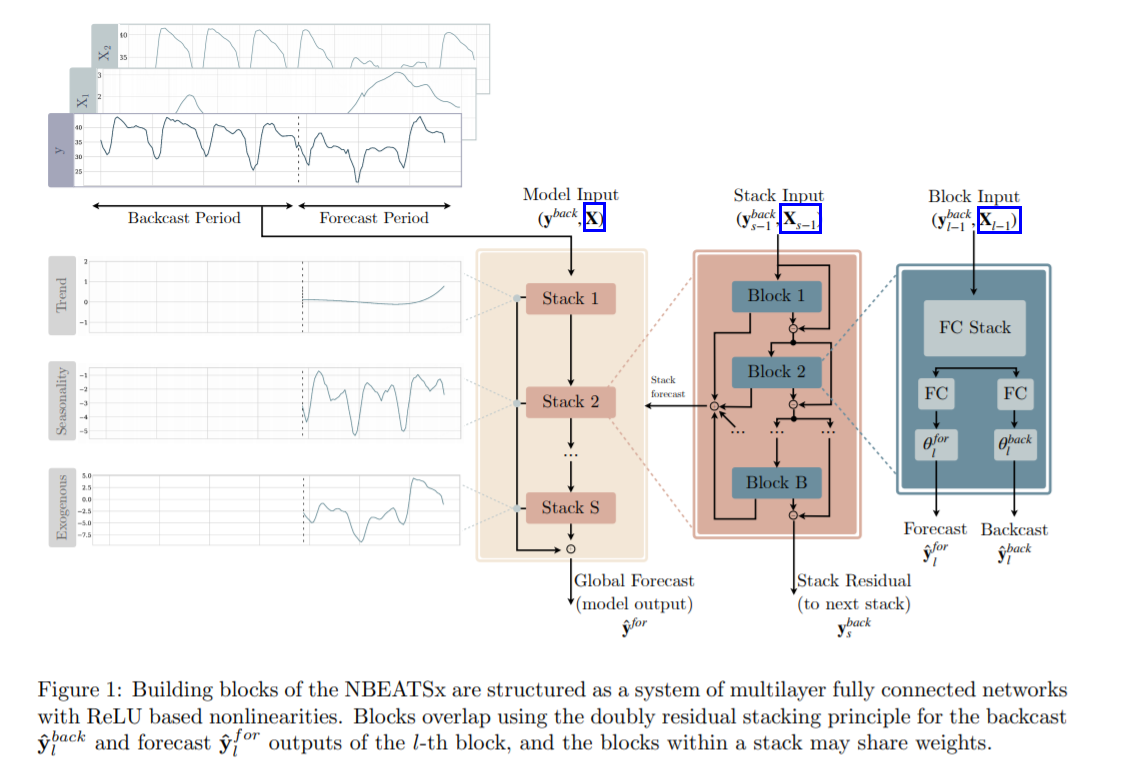

3. NBEATSx Model

decomposes the object signal by performing separate local nonlinear projection of the target data onto basis functions across its different blocks

- each block consists of FCNN, which learns expansion coefficients for back&forecast

- backcast : used to clean the inputs of subsequent blocks

- forecast : summed to compose the final prediction

-

notation

-

objective signal : \(\mathbf{y}\)

-

inputs for the model = 1) + 2)

-

1) backcast window vector \(\mathbf{y}^{\text {back }}\) of length \(L\)

( \(L\) = length of the lags )

-

2) forecast window vector \(\mathbf{y}^{\text {for }}\) of length \(H\)

( \(H\) = forecast horizon )

-

-

-

original NBEATS : admits \(\mathbf{y}^{\text {back }}\)

NBEATSx : admits \(\mathbf{y}^{\text {back }}\) & \(\mathbf{X}\) ( =exogenous matrix )

(1) Stacks and Blocks

NBEATSx is composed by S stacks of B blocks

( first transformation )

\(\mathbf{h}_{l} =\mathbf{F C N N}_{l}\left(\mathbf{y}_{l-1}^{b a c k}, \mathbf{X}_{l-1}\right)\).

- \(\boldsymbol{\theta}_{l}^{f o r} =\mathbf{L I N E A R}^{f o r}\left(\mathbf{h}_{l}\right)\).

- \(\boldsymbol{\theta}_{l}^{\text {back }}=\mathbf{L I N E A R}^{\text {back }}\left(\mathbf{h}_{l}\right)\).

( second transformation )

\(\hat{\mathbf{y}}_{l}^{b a c k}=\sum_{i=1}^{ \mid \theta_{l}^{b c k} \mid } \theta_{l, i}^{\text {back }} \mathbf{v}_{l, i}^{\text {back }} \equiv \boldsymbol{\theta}_{l}^{\text {back }} \mathbf{V}_{l}^{\text {back }}\).

\(\hat{\mathbf{y}}_{l}^{f o r}=\sum_{i=1}^{ \mid \boldsymbol{\theta}_{l}^{\text {for}} \mid } \theta_{l, i}^{\text {for }} \mathbf{v}_{l, i}^{f o r} \equiv \boldsymbol{\theta}_{l}^{\text {for }} \mathbf{V}_{l}^{\text {for }}\).

- block’s basis vectors : \(\mathbf{V}_{l}^{\text {back }}\) & \(\mathbf{V}_{l}^{\text {for}}\)

(2) Residual Connections

connections between blocks :

- \(\mathbf{y}_{l}^{\text {back }}=\mathbf{y}_{l-1}^{\text {back }}-\hat{\mathbf{y}}_{l-1}^{\text {back }}\).

- \(\hat{\mathbf{y}}^{\text {for }}=\sum_{l=1}^{S \times B} \hat{\mathbf{y}}_{l}^{\text {for }}\).

이하는 NBEATS와 동일하므로 생략