Deep Adaptive Input Normalization for Time Series Forecasting (2019, 25)

Contents

- Abstract

- Introduction

- Deep Adaptive Input Normalization (DAIN)

- Adaptive Shifting layer

- Adaptive Scaling layer

- Adaptive Gating layer

0. Abstract

- DL degenerate, if data are not “properly normalized”

- data can be..

- 1) non-stationary

- 2) multimodal- nature

- propose adaptively normalizing the input TS

1. Introduction

mostly heuristically-designed normalization

to overcome…. propose DAIN (Deep Adaptive Input Normalization)

- 1) capable of “LEARNING” how data should be normalized

- 2) “ADAPTIVELY” changing the applied normalization scheme

\(\rightarrow\) effectively handle “non-stationary” & “multi-modal” data

3 sub layers

- 1) shift the data ( centering )

- 2) scaling ( standardization )

- 3) gating ( suppressing features that are irrelevant )

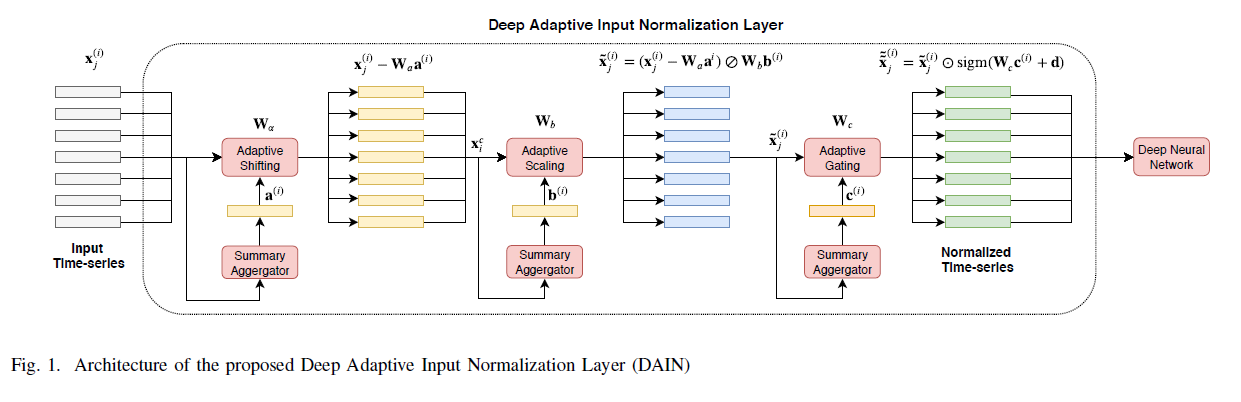

2. Deep Adaptive Input Normalization (DAIN)

Notation

- \(\left\{\mathrm{X}^{(i)} \in \mathbb{R}^{d \times L} ; i=1, \ldots, N\right\}\).

- \(\mathbf{x}_{j}^{(i)} \in \mathbb{R}^{d}, j=1,2, \ldots, L\).

- \(N\) data points (TS)

- \(L\) : length

- \(d\) : # of features

Normalization

- \(\tilde{\mathbf{x}}_{j}^{(i)}=\left(\mathbf{x}_{j}^{(i)}-\boldsymbol{\alpha}^{(i)}\right) \oslash \boldsymbol{\beta}^{(i)},\).

- ex) \(z\)-score normalization

- \(\boldsymbol{\alpha}=\left[\mu_{1}, \mu_{2}, \ldots, \mu_{d}\right]\).

- \(\boldsymbol{\beta}^{(i)}=\boldsymbol{\beta}=\left[\sigma_{1}, \sigma_{2}, \ldots, \sigma_{d}\right]\).

Propose to “dynamically estimate” these quantities

& “separately” normalize each TS, by “implicitly estimating” the distn

(1) Adaptive Shifting Layer

Shifting Operator : \(\alpha^{(i)}=\mathbf{W}_{a} \mathbf{a}^{(i)} \in \mathbb{R}^{d}\)

- summary representation : \(\mathbf{a}^{(i)}=\frac{1}{L} \sum_{j=1}^{L} \mathbf{x}_{j}^{(i)} \in \mathbb{R}^{d}\)

- \(\mathbf{W}_{a} \in \mathbb{R}^{d \times d}\) : weight matrix

Allows for exploiting possible correlations between different features

(2) Adaptive Scaling Layer

Scaling Operator : \(\boldsymbol{\beta}^{(i)}=\mathbf{W}_{b} \mathbf{b}^{(i)} \in \mathbb{R}^{d}\)

- updated summary representation : \(b_{k}^{(i)}=\sqrt{\frac{1}{L} \sum_{j=1}^{L}\left(x_{j, k}^{(i)}-\alpha_{k}^{(i)}\right)^{2}}, \quad k=1,2, \ldots, d\)

- \(\mathbf{W}_{b} \in \mathbb{R}^{d \times d}\) : weight matrix

(3) Adaptive Gating Layer

\(\tilde{\tilde{\mathbf{x}}}_{j}^{(i)}=\tilde{\mathbf{x}}_{j}^{(i)} \odot \gamma^{(i)}\).

- \(\gamma^{(i)}=\operatorname{sigm}\left(\mathbf{W}_{c} \mathbf{c}^{(i)}+\mathbf{d}\right) \in \mathbb{R}^{d}\).

- \(\mathbf{W}_{c} \in \mathbb{R}^{d \times d}\) & \(\mathrm{d} \in \mathbb{R}^{d}\) : weight

- \(\mathbf{c}^{(i)}=\frac{1}{L} \sum_{j=1}^{L} \tilde{\mathbf{x}}_{j}^{(i)} \in \mathbb{R}^{d}\).

Suppress features that are not relevant

Summary

- \(\alpha^{(i)}, \beta^{(i)}, \gamma^{(i)}\) are dependent on current ‘local’ data on window \(i\)

-

‘global’ estimates of \(\mathbf{W}_{a}, \mathbf{W}_{b}, \mathbf{W}_{c}, \mathbf{d}\) , that are trained using multiple samples on time-series, \(\left\{\mathbf{X}^{(i)} \in \mathbb{R}^{d \times L} ; i=1, \ldots, M\right\}\)

- no additional training required! (end-to-end)