Non-stationary Transformers: Exploring the Stationarity in Time Series Forecasting (NeurIPS 2022)

https://github.com/thuml/Nonstationary_Transformers.

Contents

- Abstract

- Introduction

- Related Works

- Deep Models for TSF

- Stationarization for TSF

- Non-stationary Transformers

- Series Stantionarization

- De-stationary Attention

- Experiments

- Experimental Setups

- Main Results

- Ablation Study

Abstract

Previous studies : use stationarization to attenuate the non-stationarity of TS

\(\rightarrow\) can be less instructive for real-world TS

Non-stationary Transformers

Two interdependent modules:

- (1) Series Stationarization

- unifies the statistics of each input

- converts the output with restored statistics

- (2) De-stationary Attention

- to address over-stationarization problem

- use attention to recover the intrinsic non-stationary information into temporal dependencies

1. Introduction

Non-stationarity of data

- continuous change of statistical properties and joint distribution over time ( makes it less predictable [6, 14] )

- generally acknowledged to pre-process the time series by stationarization [24, 27, 15]

However, non-stationarity is the inherent property

\(\rightarrow\) also good guidance for discovering temporal dependencies

Example) Figure 1

-

( Figure 1 (a) ) Transformers can capture distinct temporal dependencies from different series

-

( Figure 1 (b) ) Transformers trained on the stationarized series tend to generate indistinguishable attentions

\(\rightarrow\) over-stationarization problem

- unexpected side-effect … makes Transformers fail to capture eventful temporal dependencies

Key question:

- (1) how to attenuate TS non-stationarity towards better predictability

- (2) mitigate the over-stationarization problem?

Proposal:

- explore the effect of stationarization in TSF

- propose Non-stationary Transformers

Non-stationary Transformers

two interdependent modules:

- (1) Series Stationarization

- to increase the predictability of nonstationary series

- (2) De-stationary Attention

- to alleviate over-stationarization

a) Series Stationarization

- simple normalization strategy

- to unify the key statistics of each series without extra parameters

b) De-stationary Attention

- approximates the attention of unstationarized data

- compensates the intrinsic non-stationarity of raw series

2. Related Works

(1) Deep Models for TSF

- pass

(2) Stationarization for TSF

Adaptive Norm [24]

- applies z-score normalization for each series fragment by global statistics

DAIN [27]

- employs a nonlinear NN to adaptively stationarize TS

RevIN [15]

- two-stage instance normalization

Non-stationary Transformer

- directly stationarizing TS will damage the model’s capability of modeling specific temporal dependency.

- in addition to the (1) stationarization, further develops (2) De-stationary Attention to bring the intrinsic non-stationarity of the raw series back to attention.

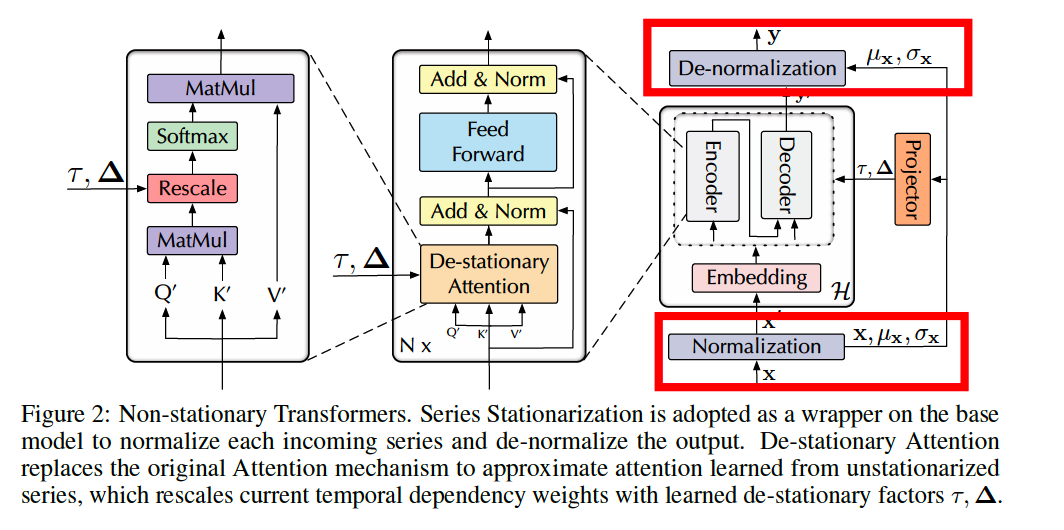

3. Non-stationary Transformers

(1) Series Stationarization

Straightforward but effective design to wrap Transformers as the base model without extra parameters

2 corresponding operations:

- (1) Normalization module

- (2) De-normalization module

(2) De-stationary Attention

Non-stationarity of the original TS cannot be fully recovered only by Denormalization!

De-stationary Attention mechanism

- approximate the attention that is obtained without stationarization

- discover the particular temporal dependencies from original non-stationary TS

Self-Attention: \(\operatorname{Attn}(\mathbf{Q}, \mathbf{K}, \mathbf{V})=\operatorname{Softmax}\left(\frac{\mathbf{Q K}^{\top}}{\sqrt{d_k}}\right) \mathbf{V}\).

Bring the vanished non-stationary information back to its calculation

-

approximate the

- positive scaling scalar \(\tau=\sigma_{\mathbf{x}}^2 \in \mathbb{R}^{+}\)

- shifting vector \(\boldsymbol{\Delta}=\mathbf{K} \mu_{\mathbf{Q}} \in \mathbb{R}^{S \times 1}\),

which are defined as de-stationary factors.

-

try to learn de-stationary factors directly from the statistics of unstationarized \(\mathbf{x}, \mathbf{Q}\) and \(\mathbf{K}\) by MLP

\(\log \tau=\operatorname{MLP}\left(\sigma_{\mathbf{x}}, \mathbf{x}\right)\).

\(\boldsymbol{\Delta}=\operatorname{MLP}\left(\mu_{\mathbf{x}}, \mathbf{x}\right)\). \(\operatorname{Attn}\left(\mathbf{Q}^{\prime}, \mathbf{K}^{\prime}, \mathbf{V}^{\prime}, \tau, \boldsymbol{\Delta}\right)=\operatorname{Softmax}\left(\frac{\tau \mathbf{Q}^{\prime} \mathbf{K}^{\prime}+\mathbf{1} \boldsymbol{\Delta}^{\top}}{\sqrt{d_k}}\right) \mathbf{V}^{\prime}\).

4. Experiments

(1) Experimental Setups

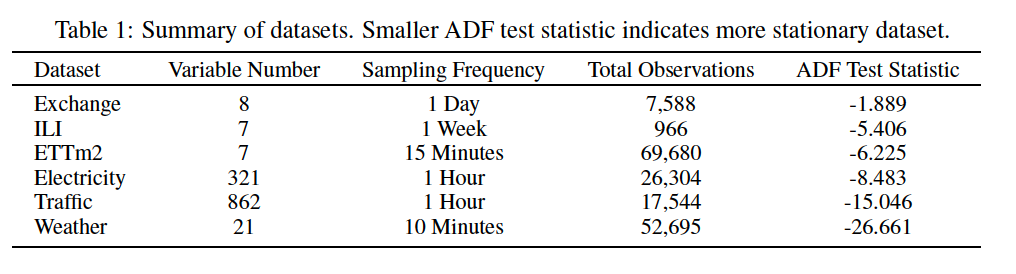

a) Datasets

- Electricity

- ETT datasets

- IExchange

- ILI

- Traffic

- Weather

b) Degree of stationarity

Augmented Dick-Fuller (ADF) test statistic

- small value = high stationarity

c) Baselines

- pass

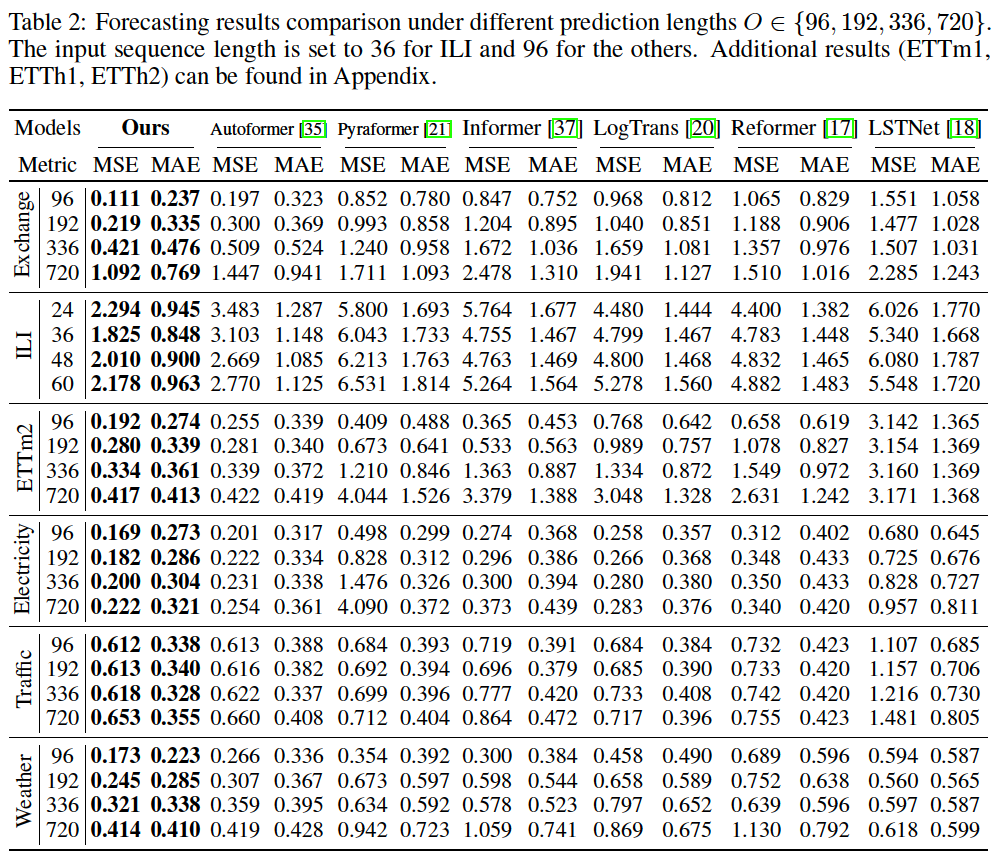

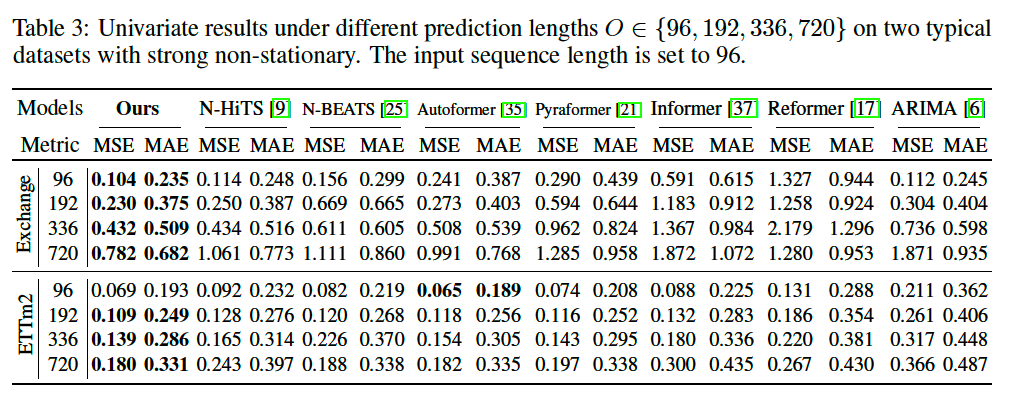

(2) Main Results

a) Forecasting

MTS Forecasting

UTS Forecasting

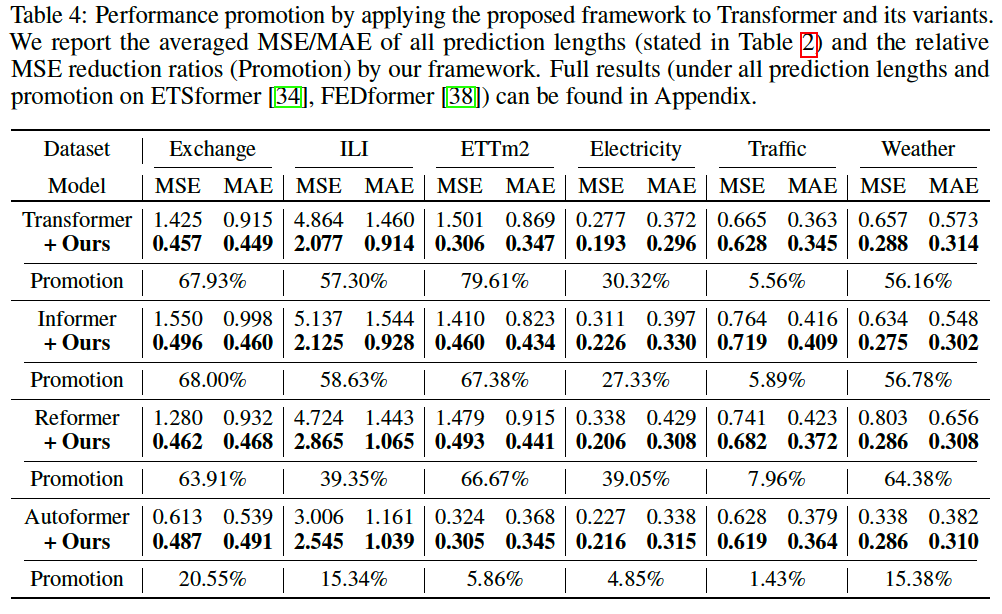

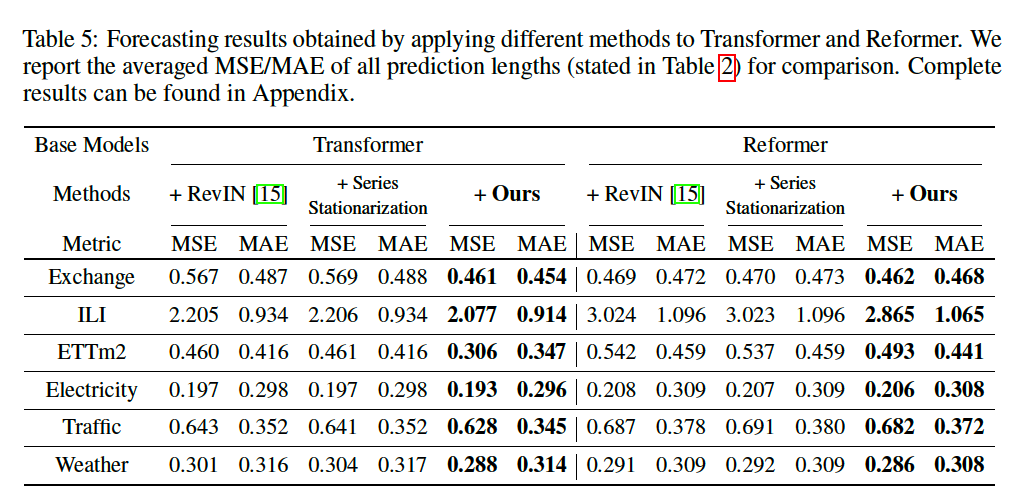

b) Framework Generality

Conclusion: Non-stationary Transformer is an effective and lightweight framework that can be widely applied to Transformer-based models and enhances their non-stationary predictability

(3) Ablation Study

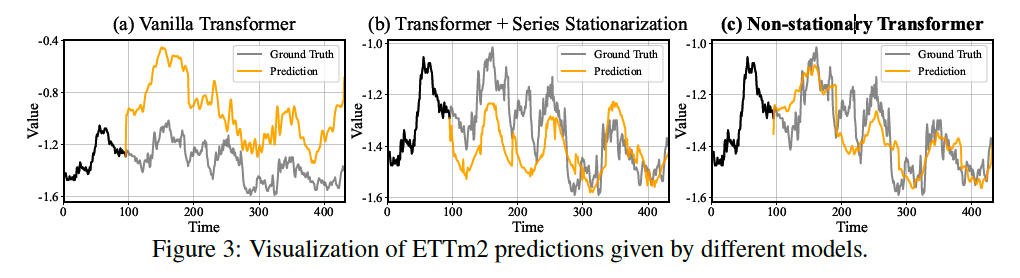

a) Quality evaluation

Dataset: ETTm2

Models:

- vanilla Transformer

- Transformer with only Series Stationarization

- Non-stationary Transformer

b) Quantitative performance

(3) Model Analysis

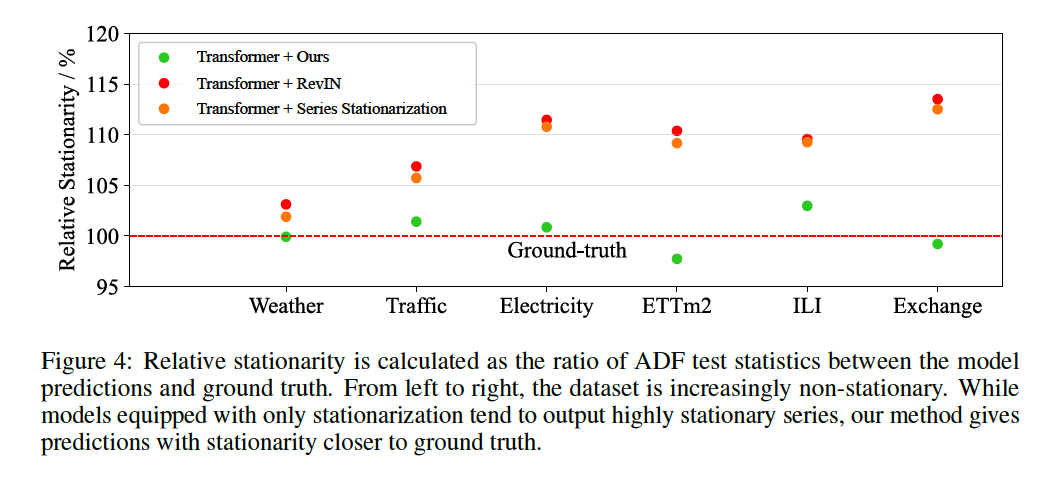

a) Over-stationarization problem

Transformers with ….

- v1) Transformer + Ours ( = Non-stationary Transformer )

- v2) Transformer + RevIN

- v3) Transformer + Series Stationarization

Result

- v2 & v3) tend to output series with unexpected high degree of stationarity