Deep Adaptive Input Normalization for Price Forecasting using Limit Order Book Data (2019)

https://github.com/passalis/dain.

Contents

- Abstract

- Introduction

- DAIN

Abstract

DAIN

- simple, yet effective, neural layer

- capable of adaptively normalizing the input time series

-

take into account the distribution of the data

- trained in an end-to-end fashion using back-propagation

Key point

“learns how to perform normalization for a given task, instead of using a fixed normalization scheme”

- can be directly applied to any new TS without requiring re-training

1. Introduction

Deep Adaptive Input Normalization (DAIN): capable of

- a) learning how the data should be normalized

- b) adaptively changing the applied normalization scheme during inference

- according to the distribution of the measurements of the current TS

\(\rightarrow\) effectively handle non-stationary and multimodal data

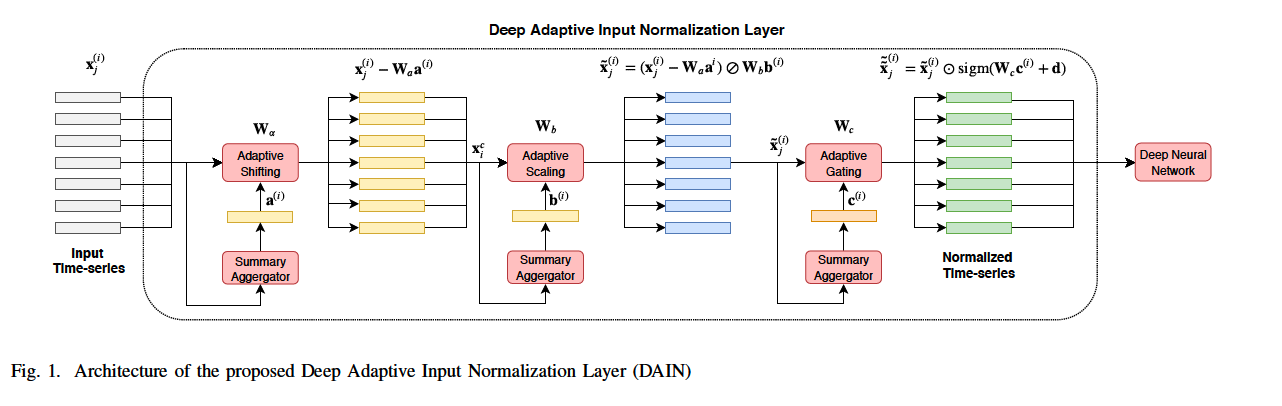

3 sublayers

- (layer 1: centering) shifting the data

- (layer 2: standardization) linearly scaling the data

- (layer 3: gating) performing gating, i.e., nonlinearly suppressing features that are irrelevant or not useful

\(\rightarrow\) the applied normalization is TRAINABLE

2. Deep Adaptive Input Normalization (DAIN)

\(N\) time series: \(\left\{\mathbf{X}^{(i)} \in \mathbb{R}^{d \times L} ; i=1, \ldots, N\right\}\)

- \(\mathbf{x}_j^{(i)} \in \mathbb{R}^d, j=1,2, \ldots, L\) : \(d\) features observed at time point \(j\) in time series \(i\).

Z-score normalization

-

most widely used form of normalization

-

if data were not generated by a unimodal Gaussian distribution…

\(\rightarrow\) lead to sub-optimal results

\(\rightarrow\) should be normalized in an mode-aware fashion

Goal : learn how to shift & scale

-

\(\tilde{\mathbf{x}}_j^{(i)}=\left(\mathbf{x}_j^{(i)}-\boldsymbol{\alpha}^{(i)}\right) \oslash \boldsymbol{\beta}^{(i)}\).

-

ex) z-score normalization

- \(\boldsymbol{\alpha}^{(i)}=\) \(\boldsymbol{\alpha}=\left[\mu_1, \mu_2, \ldots, \mu_d\right]\) and \(\boldsymbol{\beta}^{(i)}=\boldsymbol{\beta}=\left[\sigma_1, \sigma_2, \ldots, \sigma_d\right]\),

- where \(\mu_k\) and \(\sigma_k\) refer to the global average and standard deviation of the \(k\)-th input feature

- \(\boldsymbol{\alpha}^{(i)}=\) \(\boldsymbol{\alpha}=\left[\mu_1, \mu_2, \ldots, \mu_d\right]\) and \(\boldsymbol{\beta}^{(i)}=\boldsymbol{\beta}=\left[\sigma_1, \sigma_2, \ldots, \sigma_d\right]\),

Procedure

- step 1-1) summary representation of the TS

- \(\mathbf{a}^{(i)}=\frac{1}{L} \sum_{j=1}^L \mathbf{x}_j^{(i)} \in \mathbb{R}^d\).

- average all the \(L\) measurements

- provides an initial estimation for the mean

- \(\mathbf{a}^{(i)}=\frac{1}{L} \sum_{j=1}^L \mathbf{x}_j^{(i)} \in \mathbb{R}^d\).

- step 1-2) generate shifting operator \(\boldsymbol{\alpha}^{(i)}\)

- \(\boldsymbol{\alpha}^{(i)}=\mathbf{W}_a \mathbf{a}^{(i)} \in \mathbb{R}^d\).

- linear transformation of \(\mathbf{a}^{(i)}\)

- where \(\mathbf{W}_a \in \mathbb{R}^{d \times d}\) is the weight matrix of the first NN layer

- ( called adaptive shifting layer )

- \(\because\) estimates how the data must be shifted before feeding them to the network.

- allows for exploiting possible correlations between different features to perform more robust normalization.

- \(\boldsymbol{\alpha}^{(i)}=\mathbf{W}_a \mathbf{a}^{(i)} \in \mathbb{R}^d\).

-

step 2-1) update (2nd) summary representations

-

\(b_k^{(i)}=\sqrt{\frac{1}{L} \sum_{j=1}^L\left(x_{j, k}^{(i)}-\alpha_k^{(i)}\right)^2}, \quad k=1,2, \ldots, d\).

( corresponds to stddev )

-

- step 2-2) generate scaling operator \(\boldsymbol{\beta}^{(i)}\)

- \(\boldsymbol{\beta}^{(i)}=\mathbf{W}_b \mathbf{b}^{(i)} \in \mathbb{R}^d\).

- where \(\mathbf{W}_b \in \mathbb{R}^{d \times d}\) is the weight matrix the scaling layer

- ( called adaptive scaling layer )

- \(\because\) estimates how the data must be scaled before feeding them to the network.

- \(\boldsymbol{\beta}^{(i)}=\mathbf{W}_b \mathbf{b}^{(i)} \in \mathbb{R}^d\).

- step 2-3) normalize using \(\alpha\) and \(\beta\)

- \(\tilde{\mathbf{x}}_j^{(i)}=\left(\mathbf{x}_j^{(i)}-\boldsymbol{\alpha}^{(i)}\right) \oslash \boldsymbol{\beta}^{(i)}\).

-

step 3) adaptive gating layer

- suppressing features that are not relevant or useful

- \(\tilde{\tilde{\mathbf{x}}}_j^{(i)}=\tilde{\mathbf{x}}_j^{(i)} \odot \gamma^{(i)}\),

- where \(\gamma^{(i)}=\operatorname{sigm}\left(\mathbf{W}_c \mathbf{c}^{(i)}+\mathbf{d}\right) \in \mathbb{R}^d\)

- where \(\mathbf{W}_c \in\) \(\mathbb{R}^{d \times d}\) and \(\mathbf{d} \in \mathbb{R}^d\) are the parameters of the gating layer

- where \(\mathbf{c}^{(i)}\) is a (3rd) summary representation : \(\mathbf{c}^{(i)}=\frac{1}{L} \sum_{j=1}^L \tilde{\mathbf{x}}_j^{(i)} \in \mathbb{R}^d\)

- where \(\gamma^{(i)}=\operatorname{sigm}\left(\mathbf{W}_c \mathbf{c}^{(i)}+\mathbf{d}\right) \in \mathbb{R}^d\)

Summary: \(\alpha^{(i)}, \beta^{(i)}, \gamma^{(i)}\) are dependent on ..

- current ‘local’ data on window \(i\)

- ‘global’ estimates of \(\mathbf{W}_a, \mathbf{W}_b, \mathbf{W}_c, \mathbf{d}\)