DeepAR : Probabilistic Forecasting with Autoregressive Recurrent Networks (2019)

Contents

- Abstract

- Introduction

- Model

- Likelihood model

- Training

- Scale Handling

- Features

0. Abstract

Probabilistic Forecasting : 비즈니스에서 핵심!

DeepAR을 제안한다

- produce “accurate probabilistic forecast”

- based on training an auto-regressive RNN

1. Introduction

Prevalent Forecasting method

- setting of forecasting “individual or small groups” of time series

- each time series are independently estimated

- model is manually selected

- mostly based on..

- 1) Box-Jenkins methodology

- 2) Exponential Smoothing Techniques

- 3) State space models

Recent years

- faced with forecasting “thousands/millions of related time series”

- use data from related time series

- more complex models (w.o overfitting)

- alleviate time & labor intensive manual feature engineering

DeepAR

- learns a global model

- from historical data of all time series

- build upon deep learning

- tailors a similar LSTM-based RNN architecture

- to solve probabilistic forecasting problem

[ Contributions ]

- propose RNN architecture for probabilistic forecasting,

- incorporate a negative Binomial likelihood for count data

- special treatment for the case when magnitudes of the time series vary widely

- experiment on real world data

Key Advantages of DeepAR

-

learns seasonal behavior and dependencies on given covariates across time series

\(\rightarrow\) minimal manual feature engineering is needed to capture complex, group-dependent behavior

-

makes probabilistic forecasts in the form of Monte Carlo samples

\(\rightarrow\) can be used to compute consistent quantile estimates

-

by learning from similar items, able to provide forecasts for items with little or no history at all

-

does not assume Gaussian noise, but can incorporate a wide range of likelihood functions

\(\rightarrow\) allow the user to choose one that is appropriate for the statistical properties of the data

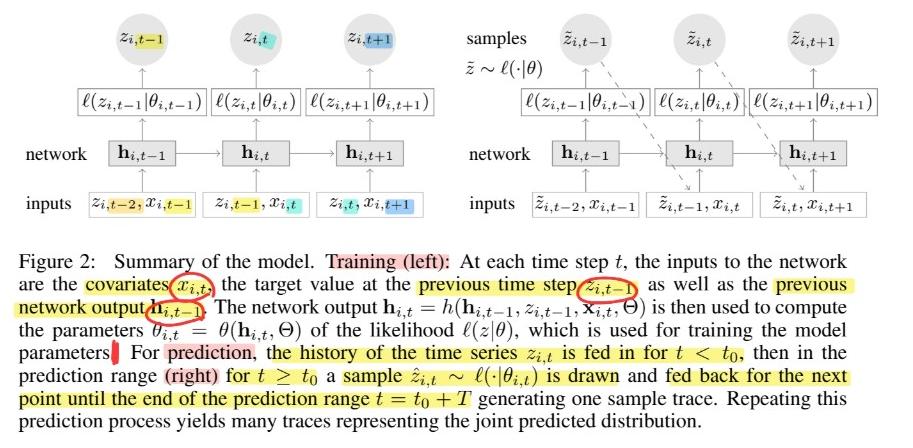

2. Model

Notation

- \(z_{i, t}\) : value of time series \(i\) at time \(t\)

- \(\mathbf{x}_{i, 1: T}\) : covariates that are assumed to be known for all time points

- goal : model \(P\left(\mathbf{z}_{i, t_{0}: T} \mid \mathbf{z}_{i, 1: t_{0}-1}, \mathbf{x}_{i, 1: T}\right)\)

- \(\left[1, t_{0}-1\right]\) : conditioning range

- \(\left[t_{0}, T\right]\) : prediction range

based on Autoregressive Recurrent Network architecture

model distribution : \(Q_{\Theta}\left(\mathbf{z}_{i, t_{0}: T} \mid \mathbf{z}_{i, 1: t_{0}-1}, \mathbf{x}_{i, 1: T}\right)\)

-

factorized as

\(Q_{\Theta}\left(\mathbf{z}_{i, t_{0}: T} \mid \mathbf{z}_{i, 1: t_{0}-1}, \mathbf{x}_{i, 1: T}\right)=\prod_{t=t_{0}}^{T} Q_{\Theta}\left(z_{i, t} \mid \mathbf{z}_{i, 1: t-1}, \mathbf{x}_{i, 1: T}\right)=\prod_{t=t_{0}}^{T} \ell\left(z_{i, t} \mid \theta\left(\mathbf{h}_{i, t}, \Theta\right)\right)\).

-

\(\mathbf{h}_{i, t}=h\left(\mathbf{h}_{i, t-1}, z_{i, t-1}, \mathbf{x}_{i, t}, \Theta\right)\).

Information about the observations in the conditioning range \(\mathbf{z}_{i, 1: t_{0}-1}\)

is transferred to the prediction range through the initial state \(\mathbf{h}_{i, t_{0}-1}\)

Given the model parameters \(\Theta\)…

can obtain joint samples \(\tilde{\mathbf{z}}_{i, t_{0}: T} \sim\) \(Q_{\Theta}\left(\mathbf{z}_{i, t_{0}: T} \mid \mathbf{z}_{i, 1: t_{0}-1}, \mathbf{x}_{i, 1: T}\right)\) via ancestral sampling

- step 1) obtain \(\mathbf{h}_{i, t_{0}-1}\) by \(\mathbf{h}_{i, t}=h\left(\mathbf{h}_{i, t-1}, z_{i, t-1}, \mathbf{x}_{i, t}, \Theta\right)\)

- for \(t=1,...,t_0\)

- step 2) sample \(\tilde{z}_{i, t} \sim \ell\left(\cdot \mid \theta\left(\tilde{\mathbf{h}}_{i, t}, \Theta\right)\right)\)

- for \(t=t_0,...T\)

- where \(\tilde{\mathbf{h}}_{i, t}=h\left(\mathbf{h}_{i, t-1}, \tilde{z}_{i, t-1}, \mathbf{x}_{i, t}, \Theta\right)\)

\(\rightarrow\) samples can be used to compute quantities of interests ( ex. quantile )

(1) Likelihood model

two choices :

- 1) (real-valued) Gaussian

- 2) (count data) Negative-binomial

a) Gaussian

mean and standard deviation, \(\theta=(\mu, \sigma)\)

\(\begin{aligned} \ell_{\mathrm{G}}(z \mid \mu, \sigma) &=\left(2 \pi \sigma^{2}\right)^{-\frac{1}{2}} \exp \left(-(z-\mu)^{2} /\left(2 \sigma^{2}\right)\right) \\ \mu\left(\mathbf{h}_{i, t}\right) &=\mathbf{w}_{\mu}^{T} \mathbf{h}_{i, t}+b_{\mu} \quad \text { and } \quad \sigma\left(\mathbf{h}_{i, t}\right)=\log \left(1+\exp \left(\mathbf{w}_{\sigma}^{T} \mathbf{h}_{i, t}+b_{\sigma}\right)\right) \end{aligned}\).

b) Negative-binomial

mean \(\mu \in \mathbb{R}^{+}\)and a shape parameter \(\alpha \in \mathbb{R}^{+}\)

\(\begin{aligned} \ell_{\mathrm{NB}}(z \mid \mu, \alpha) &=\frac{\Gamma\left(z+\frac{1}{\alpha}\right)}{\Gamma(z+1) \Gamma\left(\frac{1}{\alpha}\right)}\left(\frac{1}{1+\alpha \mu}\right)^{\frac{1}{\alpha}}\left(\frac{\alpha \mu}{1+\alpha \mu}\right)^{z} \\ \mu\left(\mathbf{h}_{i, t}\right) &=\log \left(1+\exp \left(\mathbf{w}_{\mu}^{T} \mathbf{h}_{i, t}+b_{\mu}\right)\right) \quad \text { and } \quad \alpha\left(\mathbf{h}_{i, t}\right)=\log \left(1+\exp \left(\mathbf{w}_{\alpha}^{T} \mathbf{h}_{i, t}+b_{\alpha}\right)\right) \end{aligned}\).

(2) Training

given data

- 1) \(\left\{\mathbf{z}_{i, 1: T}\right\}_{i=1, \ldots, N}\)

- 2) associated covariates \(\mathbf{x}_{i, 1: T}\)

optimize parameters \(\Theta\) by maximizing log-likelihood :

- \(\mathcal{L}=\sum_{i=1}^{N} \sum_{t=t_{0}}^{T} \log \ell\left(z_{i, t} \mid \theta\left(\mathbf{h}_{i, t}\right)\right)\).

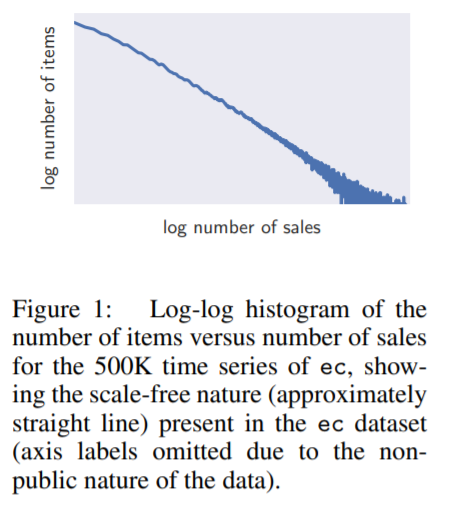

(3) Scale Handling

Problem : data that shows power-law of scales as…

Two problems caused by this :

Problem 1

- network has to learn to scale the input & then invert this scaling at the output

Solution 1

- divide the autoregressive inputs \(z_{i,t}\) ( or \(\tilde{z_{i,t}}\) ) by item-dependent scale factor \(\nu_i\)

- multiply the scale-dependent likelihood params by the same factor

- ex) for Neg-binom…

- \(\mu=\nu_{i} \log \left(1+\exp \left(o_{\mu}\right)\right)\).

- \(\alpha=\log \left(1+\exp \left(o_{\alpha}\right)\right) / \sqrt{\nu_{i}}\).

- where \(o_{\mu}, o_{\alpha}\) are outputs of NN

- for real-valued data, just normalize in advance!

Problem 2

-

imbalance in the data

\(\rightarrow\) stochastic optimization procedure visit small number time-series with a large scale very infrequently

Solution 2

- sample the examples non-uniformly during training

- probability of selecting a window from an example with scale \(\nu_i\) is proportional to \(\nu_i\)

(4) Features

covariates \(\mathbf{x_{i,t}}\) can be item-dependent/independent