Probabilistic Forecasting with Temporal Convolutional Neural Network (2020)

Contents

- Abstract

- Introduction

- Classical forecasting methods

- DL based methods

- Dilated causal convolutional architectures

- Auto vs Non-Autoregressive

- (proposal) DeepTCN

- Method

- NN architecture

- Encoder : Dilated Causal Convolutions

- Decoder : Residual Neural Network

- Probabilistic forecasting framework

- Input Features

0. Abstract

probabilistic forecasting, baed on CNN

- under both 1) parametric and 2) non-parametric settings

- stacked residual blocks, based on dilated causal convolutional nets

- able to learn complex patterns, such as seasonality, holiday effects

1. Introduction

instead of predicting individual/small number of t.s…

\(\rightarrow\) needs to predict thousands/millions of related t.s

1) Classical forecasting methods

- ARIMA (Autoregressive Integrated Moving Average)

- exponential smoothing ( for univariate base-level forecasting )

- ARIMAX = ARIMA + eXogeneous variable

\(\rightarrow\) however, working with thousands/millions of series requires prohibitive labor and computing resources for parameter estimation & not applicable when historical data is sparse / unavailable

2) DL based methods

- RNN

- Seq2Seq

- GRU

\(\rightarrow\) BPTT hampers efficient computations

3) Dilated causal convolutional architectures

-

Wavenet : alternative for modeling sequential data

-

staking layers of DCC … receptive fields can be increased

( w.o violating temporal orders )

-

can be performed in parallel

4) Auto vs Non-Autoregressive

Autoregressive models

- ex) seq2seq, wavenet

- factorize the joint distn

- one-step-ahead prediction approach

Non-Autoregressive models

- direct prediction strategy

- usually better performances

- avoid error accumulation

- can be parallelized

5) (proposal) DeepTCN

Deep Temporal Convolutional Network

-

non-autoregressive probabilistic forecasting

-

Contributions

- 1) CNN-based forecasting framework

- 2) high scalability & extensibility

- 3) very flexible & include exogenous covariates

- 4) both point & probabilistic forecasting

2. Method

Notation

- \(\mathbf{y}_{1: t}=\left\{y_{1: t}^{(i)}\right\}_{i=1}^{N}\) : set of time series ( Multivariate…number of time series \(N\) )

- \(\mathbf{y}_{(t+1):(t+\Omega)}=\left\{y_{(t+1):(t+\Omega)}^{(i)}\right\}_{i=1}^{N}\) : future time series

- \(t\) : length of historical observations

- \(\Omega\) : length of forecasting horizon

- goal : model the conditional distribution of the future time series \(P\left(\mathbf{y}_{(t+1):(t+\Omega)} \mid \mathbf{y}_{1: t}\right)\)

1) Classical generative models

- factorize the joint probability

- \(P\left(\mathbf{y}_{(t+1):(t+\Omega)} \mid \mathbf{y}_{1: t}\right)=\prod_{\omega=1}^{\Omega} p\left(\mathbf{y}_{t+\omega} \mid \mathbf{y}_{1: t+\omega-1}\right)\).

- challenges

- 1) efficiency issue

- 2) error accumulation

2) Our framework

- joint distn DIRECTLY

- \(P\left(\mathbf{y}_{(t+1):(t+\Omega)} \mid \mathbf{y}_{1: t}\right)=\prod_{\omega=1}^{\Omega} p\left(\mathbf{y}_{t+\omega} \mid \mathbf{y}_{1: t}\right)\).

- important to allows covariates \(X_{t+\omega}^{(i)}\) (where \(\omega=1, \ldots, \Omega\) and \(\left.i=1, \ldots, N\right)\) t

- \(P\left(\mathbf{y}_{(t+1):(t+\Omega)} \mid \mathbf{y}_{1: t}\right)=\prod_{\omega=1}^{\Omega} p\left(\mathbf{y}_{t+\omega} \mid \mathbf{y}_{1: t}, X_{t+\omega}^{(i)}, i=1, \ldots, N\right)\).

- challenge : How to design NN that incorporate historical observations \(\mathbf{y}_{1: t}\) & covariates \(X_{t+\omega}^{(i)}\)

2-1. NN architecture

use both information… \(y_{t}^{(i)}=\nu_{B}\left(X_{t}^{(i)}\right)+n_{t}^{(i)}\).

- 1) past observation

- 2) exogenous variables

to extend dynamic regression to multiple t.s forecasting scenario…

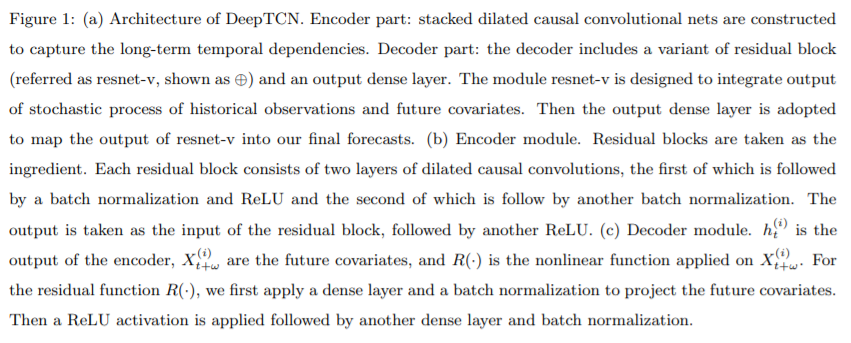

\(\rightarrow\) propose a variant of residual NN

Main difference from original ResNet : new block allows for 2 inputs

- 1) one for historical observation

- 2) one for exogenous variables

propose DeepTCN

- high-level architecture is similar to Seq2Seq framework

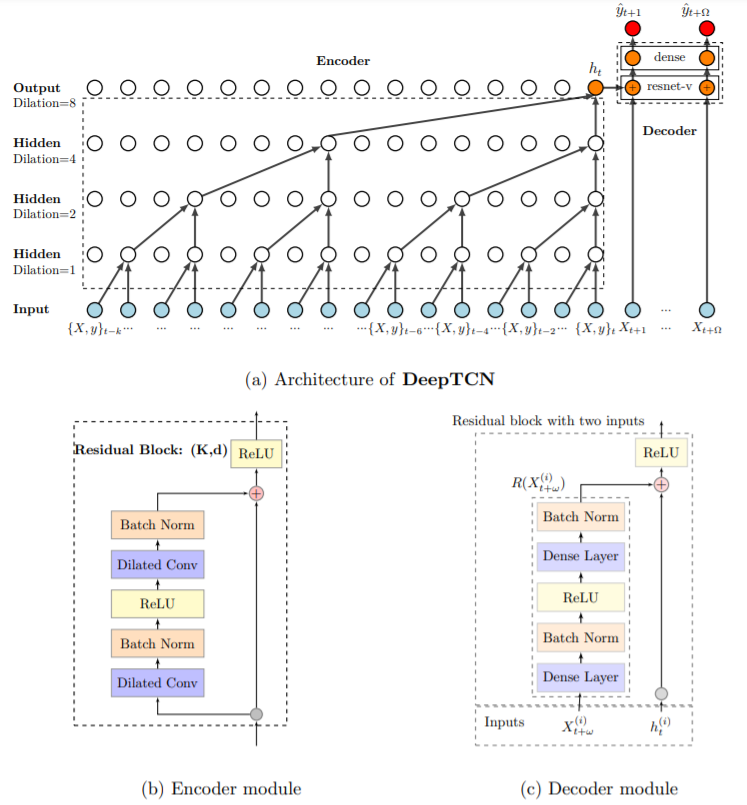

2-2. Encoder : Dilated Causal Convolutions

- use inputs, no later than \(t\)

- use skipping

- notation : \(s(t)=\left(x *_{d} w\right)(t)=\sum_{k=0}^{K-1} w(k) x(t-d \cdot k)\).

- stacking multiple Dilated Causal Convolutions :

- enable networks to have very LARGE receptive fields &

- capture LONG-range temporal dependencies with smaller number of layers

- Figure 1-a)

- \(d\) =\(\{1,2,4,8\}\)

- \(K\)=2

- receptive filed of size \(16\)

2-3. Decoder : Residual Neural Network

decoder includes 2 parts..

-

1) variant of residual neural network ( = resnet-v )

-

2) dense layer

- maps output of 1) into probabilistic forecast

-

notation : \(\delta_{t+\omega}^{(i)}=R\left(X_{t+\omega}^{(i)}\right)+h_{t}^{(i)}\)

- \(h_{t}^{(i)}\) : latent output of encoder

- \(X_{t+\omega}^{(i)}\) : future covariates

- \(\delta_{t+\omega}^{(i)}\) : latent output of resnet-v

- \(R(\cdot)\) : residual function

-

output dense layer maps the latent variable \(\delta_{t+\omega}^{(i)}\) to produce the final output \(Z\)

( = probabilistic estimation of interest )

2-4. Probabilistic forecasting framework

- output dense layer produce \(m\) outputs : \(Z=\left(z^{1}, \ldots, z^{m}\right)\)

- 2 outputs : ( mean & std ) \(Z_{t+\omega}^{(i)}=\left(\mu_{t+\omega}^{(i)}, \sigma_{t+\omega}^{(i)}\right)\).

- probabilistic forecast : \(P\left(y_{t+\omega}^{(i)}\right) \sim G\left(\mu_{t+\omega}^{(i)}, \sigma_{t+\omega}^{(i)}\right)\).

1) Non-parametric approach

- forecasts can be obtained by quantile regression

- quantile loss : \(L_{q}\left(y, \hat{y}^{q}\right)=q\left(y-\hat{y}^{q}\right)^{+}+(1-q)\left(\hat{y}^{q}-y\right)^{+}\)

- where \((y)^{+}=\max (0, y)\) and \(q \in(0,1)\)

- minimize the total quantile loss :

- \(L_{Q}=\sum_{j=1}^{m} L_{q_{j}}\left(y, \hat{y}^{q_{j}}\right)\).

2) Parametric approach

-

MLE (Maximum Likelihood Estimation)

-

loss function : negative log-likelihood

\(\begin{aligned} L_{G} &=-\log \ell(\mu, \sigma \mid y) \\ &=-\log \left(\left(2 \pi \sigma^{2}\right)^{-1 / 2} \exp \left[-(y-\mu)^{2} /\left(2 \sigma^{2}\right)\right]\right) \\ &=\frac{1}{2} \log (2 \pi)+\log (\sigma)+\frac{(y-\mu)^{2}}{2 \sigma^{2}} \end{aligned}\).

2-5. Input Features

2 kinds of input features

- 1) time DEPENDENT

- ex) product price, day of week

- 2) time INDEPENDENT

- ex) product id, product brand, category

To capture seasonality..

- use “hour-of-the day, day-of-the-week….”