AdaRNN: Adaptive Learning and Forecasting for Time Series (CIKM 2021)

https://arxiv.org/pdf/2108.04443.pdf

https://github.com/jindongwang/transferlearning/tree/master/code/deep/adarnn

Contents

- Abstract

- Introduction

- Related Work

- TS analysis

- Distribution matching

- Problem Formulation

- AdaRNN

- Temporal Distribution Characterization (TDC)

- Temporal Distribution Matching (TDM)

Abstract

Distribution shift

- statistical properties of a TS can vary with time

Formulate the Temporal Covariate Shift (TCS) problem for TSF

Adaptive RNNs (AdaRNN)

AdaRNN is sequentially composed of 2 modules

- (1) Temporal Distribution Characterization

- aims to better characterize the distribution information in a TS

- (2) Temporal Distribution Matching

- aims to reduce the distribution mismatch in the TS

Summary : general framework with flexible distribution distances integrated.

1. Introduction

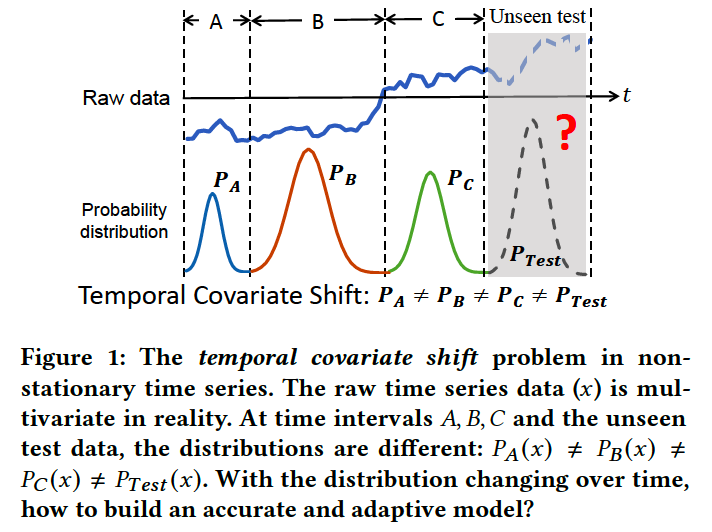

Non-stationary TS

-

Statistical properties of TS are changing over time

-

ex) Figure 1

HOWEVER … \(P(y \mid x)\) is usually considered to be unchanged!

Two main challenges of the problem

- How to characterize the distribution in the data to maximally harness the common knowledge in these varied distributions?

- How to invent an RNN-based distribution matching algorithm to maximally reduce their distribution divergence while capturing the temporal dependency?

AdaRNN

- a novel framework to learn an accurate and adaptive prediction model.

- composed of two modules.

- (1) temporal distribution characterization (TDC)

- split the training data into 𝐾 most diverse periods that are with large distribution gap inspired by the principle of maximum entropy

- (2) temporal distribution matching (TDM)

- dynamically reduce distribution divergence using RNN

- (1) temporal distribution characterization (TDC)

2. Related Work

(1) TS analysis

- pass

(2) Distribution Matching

Domain adaptation (DA)

- bridge the distribution gap

- often performs instance re-weighting or feature transfer to reduce the distribution divergence in training and test data

- ex) domain-invariant representations can be learned

Domain generalization (DG)

- also learns a domain-invariant model on multiple source domains

DA vs. DG

- DA : test data is ACCESSIBLE

- DG : test data is NOT ACCESSIBLE

3. Problem Formulation

[Problem 1] \(r\)-step ahead prediction

Notation

- \(\mathcal{D}=\left\{\mathbf{x}_i, \mathbf{y}_i\right\}_{i=1}^n\).

- \(n\) : number of TS

- where \(\mathbf{x}_i=\left\{x_i^1, \cdots, x_i^{m_i}\right\} \in \mathbb{R}^{p \times m_i}\)

- \(m_i\) : length of \(i\)-th TS

- \(p\) : number of channels

- where \(\mathbf{y}_i=\left(y_i^1, \ldots, y_i^c\right) \in \mathbb{R}^c\)

[Learn] model \(\mathcal{M}: \mathrm{x}_i \rightarrow \mathrm{y}_i\)

-

predict future \(r \in \mathbb{N}^{+}\)steps for segments \(\left\{\mathbf{x}_j\right\}_{j=n+1}^{n+r}\)

-

Previous works : all time series segments, \(\left\{\mathbf{x}_i\right\}_{i=1}^{n+r}\), are assumed to follow the same data distribution

Covariate Shift

Notation:

- train distn : \(P_{\text {train }}(\mathrm{x}, y)\)

- test distn : \(P_{\text {test }}(\mathrm{x}, y)\)

Definition of Covariate Shift

- (1) marginal probability distributions are different ( \(P_{\text {train }}(\mathbf{x}) \neq P_{\text {test }}(\mathbf{x})\) )

- (2) conditional distributions are the same ( \(P_{\text {train }}(y \mid \mathbf{x})=P_{\text {test }}(y \mid \mathbf{x})\) )

\(\rightarrow\) for NON-TS data

( TS data : Temporal Covariate Shift )

Temporal Covariate Shift (TCS)

Notation

- time series data \(\mathcal{D}\) with \(n\) labeled segments

- can be split into \(K\) periods

- i.e., \(\mathcal{D}=\left\{\mathcal{D}_1, \cdots, \mathcal{D}_K\right\}\), where \(\mathcal{D}_k=\left\{\mathrm{x}_i, \mathrm{y}_i\right\}_{i=n_k+1}^{n_{k+1}}\), \(n_1=0\) and \(n_{k+1}=n\).

Definition of Temporal Covariate Shift

- (2) all the segments in the same period \(i\) follow the same data distribution ( \(P_{\mathcal{D}_i}(\mathbf{x}, y)\) )

- (2) for different time periods \(1 \leq i \neq j \leq K\), \(P_{\mathcal{D}_i}(\mathbf{x}) \neq P_{\mathcal{D}_j}(\mathbf{x})\) and \(P_{\mathcal{D}_i}(y \mid \mathbf{x})=P_{\mathcal{D}_j}(y \mid \mathbf{x})\).

Key point: Capture the common knowledge shared among different periods of \(\mathcal{D}\)

- number of periods \(K\) and the boundaries of each period under TCS are usually unknown in practice

- need to first discover the periods by comparing their underlying data distributions such that segments in the same period follow the same data distributions.

[Problem 1] \(r\)-step ahead prediction under TCS

Given \(\mathcal{D}=\left\{\mathbf{x}_i, \mathrm{y}_i\right\}_{i=1}^n\) for training.

\(P_{\mathcal{D}_i}(\mathrm{x}, y)\) while for different time periods \(1 \leq i \neq j \leq K, P_{\mathcal{D}_i}(\mathbf{x}) \neq P_{\mathcal{D}_j}(\mathbf{x})\) and \(P_{\mathcal{D}_i}(y \mid \mathbf{x})=P_{\mathcal{D}_j}(y \mid \mathbf{x})\).

Goal:

- automatically discover the \(K\) periods in the training TS data

- learn a prediction model \(\mathcal{M}: \mathbf{x}_i \rightarrow \mathrm{y}_i\) by exploiting the commonality among different time periods, such that it makes precise predictions on the future r segments, \(\mathcal{D}_{t s t}=\left\{\mathrm{x}_j\right\}_{j=n+1}^{n+r}\).

Assumption: Test segments are in the same time period

- \(P_{\mathcal{D}_{t s t}}(\mathbf{x}) \neq P_{\mathcal{D}_i}(\mathbf{x})\) and \(P_{\mathcal{D}_{t s t}}(y \mid \mathbf{x})=P_{\mathcal{D}_i}(y \mid \mathbf{x})\) for any \(1 \leq i \leq K\).

4. AdaRNN

Consists of 2 novel algorithms ; TDC & TDM

Procedure

- step 1) use TDC to split into periods

- which fully characterize its distn information

- step 2) apply TDM to perform distribution matching among periods

- build a prediction model \(\mathcal{M}\)

Rationale behind AdaRNN

- [TDC] \(\mathcal{M}\) is expected to work under the WORST distn scenarios, where distn gaps are large

- [TDM] use the common knowledge of the learend time periods

- by matching their distns via RNNs

(1) Temporal Distribution Characterization (TDC)

Splitting the TS by solving an optimization problem

\(\begin{aligned} & \max _{0<K \leq K_0} \max _{n_1, \cdots, n_K} \frac{1}{K} \sum_{1 \leq i \neq j \leq K} d\left(\mathcal{D}_i, \mathcal{D}_j\right) \\ & \text { s.t. } \forall i, \Delta_1< \mid \mathcal{D}_i \mid <\Delta_2 ; \sum_i \mid \mathcal{D}_i \mid =n \end{aligned}\).

- \(d\) is a distance metric

- \(\Delta_1\) and \(\Delta_2\) are predefined parameters to avoid trivial solutions

- \(K_0\) is the hyperparameter to avoid over-splitting

(2) Temporal Distribution Matching (TDM)

learn the common knowledge shared by different periods

- via matching their distributions

\(\rightarrow\) \(\mathcal{M}\) is expected to generalize well on unseen test data

\(\mathcal{L}_{\text {pred }}(\theta)=\frac{1}{K} \sum_{j=1}^K \frac{1}{ \mid \mathcal{D}_j \mid } \sum_{i=1}^{ \mid \mathcal{D}_j \mid } \ell\left(\mathbf{y}_i^j, \mathcal{M}\left(\mathbf{x}_i^j ; \theta\right)\right)\).

- where \(\left(\mathrm{x}_i^j, \mathrm{y}_i^j\right)\) denotes the \(i\)-th labeled segment from period \(\mathcal{D}_j\)

Distribution matching is usually performed on high-level representations

-

on the final outputs of the cell of RNN models

( use \(\mathbf{H}=\left\{\mathbf{h}^t\right\}_{t=1}^V \in \mathbb{R}^{V \times q}\) to denote the \(V\) hidden states of an RNN with feature dimension \(q\). )

Period-wise distribution matching

- on the final hidden states for a pair \(\left(\mathcal{D}_i, \mathcal{D}_j\right)\)

\(\mathcal{L}_{d m}\left(\mathcal{D}_i, \mathcal{D}_j ; \theta\right)=d\left(\mathbf{h}_i^V, \mathbf{h}_j^V ; \theta\right)\).