Modeling Long and Short Term Temporal Patterns with DNN (2017, 496)

Contents

- Abstract

- Introduction

- Related Background

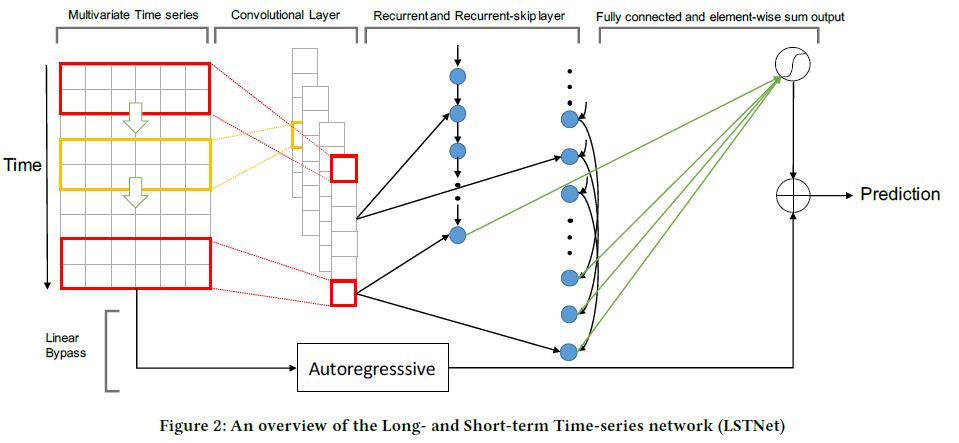

- Framework

- Problem Formulation

- Convolutional Component

- Recurrent Component

- Recurrent Skip Component

- Dense Layer

- Temporal Attention Layer

- Autoregressive Component

- Loss Function

0. Abstract

-

goal : MTS forecasting

- Temporal data = mixture of long & short term patterns

- traditional models ( GP, AR ) fails..

- propose LSTNet (Long and Short-term Time-series Network)

LSTNet

(1) use CNN & RNN to extract …

- 1) short term local dependency patterns ( among variables )

- 2) long term patterns for time series trends

(2) leverage traditional autoregressive model to tackle the scale insensitive problem

1. Introduction

MTS key point :

- how to capture & leverage “dynamics dependencies among multiple variables”

Real-world data :

- mixture of LONG & SHORT term repeating patterns

- how to capture both?

LSTNet ( Long and Short-term Time-series Network )

- 1) CNN

- to discover “LOCAL dependency patterns” among multi-dimensional input

- 2) RNN

- to capture “complex LONG term dependencies”

- 3) Recurrent-skip

- capture very long-term dependence patterns

- 4) incorporate a traditional autoregressive linear model in parallel

2. Related Background

Univariate TS

-

ARIMA ( Box-Jenkins methodology )

\(\rightarrow\) rarely used in high-dimensional MTS ( \(\because\) high computational cost )

-

VAR ( Vector Autoregression )

- VAR = AR + MTS

- widely used MTS for its simplicity

-

ignores the dependencies between output variables

-

model capacity of VAR grows ….

-

linearly over the temporal window size

-

quadratically over the number of variables

-

Others

-

SVR : non-linear

-

Ridge, LASSO …. : linear

\(\rightarrow\) practically more efficient for MTS, but fail to capture complex relationship

-

GP (Gaussian Process) : non-parametric

- can be applied to MTS

- can be used as a prior over the function space in Bayesian Inference

- high computation complexity

3. Framework

(1) Problem Formulation

interested in MTS

Notation :

- \(Y=\left\{\boldsymbol{y}_{1}, \boldsymbol{y}_{2}, \ldots, \boldsymbol{y}_{T}\right\}\) : fully observed TS

- \(\boldsymbol{y}_{t} \in \mathbb{R}^{n}\) ( \(n\) : # of variables )

- [INPUT] \(X_{T}=\left\{\boldsymbol{y}_{1}, \boldsymbol{y}_{2}, \ldots, \boldsymbol{y}_{T}\right\} \in \mathbb{R}^{n \times T}\).

- [OUTPUT] \(\hat{\boldsymbol{y}}_{T+h+1}\)

(2) Convolutional Component

[FIRST layer]

- CNN without pooling

- goal : extract SHORT term patterns & LOCAL dependencies between variables

(3) Recurrent Component

[SECOND layer]

- output of CNN is fed into “Recurrent component” & “Recurrent-skip component”

\(\begin{aligned} r_{t} &=\sigma\left(x_{t} W_{x r}+h_{t-1} W_{h r}+b_{r}\right) \\ u_{t} &=\sigma\left(x_{t} W_{x u}+h_{t-1} W_{h u}+b_{u}\right) \\ c_{t} &=R E L U\left(x_{t} W_{x c}+r_{t} \odot\left(h_{t-1} W_{h c}\right)+b_{c}\right) \\ h_{t} &=\left(1-u_{t}\right) \odot h_{t-1}+u_{t} \odot c_{t} \end{aligned}\).

(4) Recurrent-skip Component

- to solve gradient vanishing problem

\(\begin{aligned} &r_{t}=\sigma\left(x_{t} W_{x r}+h_{t-p} W_{h r}+b_{r}\right) \\ &u_{t}=\sigma\left(x_{t} W_{x u}+h_{t-p} W_{h u}+b_{u}\right) \\ &c_{t}=R E L U\left(x_{t} W_{x c}+r_{t} \odot\left(h_{t-p} W_{h c}\right)+b_{c}\right) \\ &h_{t}=\left(1-u_{t}\right) \odot h_{t-p}+u_{t} \odot c_{t} \end{aligned}\).

- \(p\) : number of hidden cells skipped

(5) Dense Layer

combine outputs of

- 1) Recurrent components ( \(h_t^R\) )

- 2) Recurrent-skip components ( \(h_t^S\) )

output of dense layer :

- \(h_{t}^{D}=W^{R} h_{t}^{R}+\sum_{i=0}^{p-1} W_{i}^{S} h_{t-i}^{S}+b\).

(6) Temporal Attention Layer

Recurrent skip layer : needs “pre-defined hyperparameter \(p\)”

\(\rightarrow\) use attention instead! ( to make weighted combinations )

\(\boldsymbol{\alpha}_{t}=\operatorname{AttnScore}\left(H_{t}^{R}, h_{t-1}^{R}\right)\).

-

attention weight \(\boldsymbol{\alpha}_{t} \in \mathbb{R}^{q}\)

-

\(H_{t}^{R}=\left[h_{t-q}^{R}, \ldots, h_{t-1}^{R}\right]\) is a matrix stacking the hidden representation of RNN column-wisely

-

\(\text{AttnScore}\) : similarity functions

ex) dot product, cosine, or parameterized by a simple multi-layer perceptron…

Weighted Context vector : \(c_{t}=H_{t} \alpha_{t}\).

Final : \(h_{t}^{D}=W\left[c_{t} ; h_{t-1}^{R}\right]+b\).

(7) Autoregressive Component

capture non-linearity by “CNN” & “RNN”

\(\rightarrow\) but…. scale of output is not sensitive to scale of inputs!

Solution : decompose the final prediction of LSTNet into a…

- 1) linear part : to deal with local scaling issue ( \(h_{t}^{L}\) )

- use AR model for this!

- \(h_{t, i}^{L}=\sum_{k=0}^{q^{a r}-1} W_{k}^{a r} \boldsymbol{y}_{t-k, i}+b^{a r}\).

- 2) non-linear part : containing recurring patterns ( \(h_{t}^{D}\) )

Final Prediction : \(\hat{Y}_{t}=h_{t}^{D}+h_{t}^{L}\)

(8) Loss Function

\(\underset{\Theta}{\operatorname{minimize}} \sum_{t \in \Omega_{\text {Train }}} \mid \mid Y_{t}-\hat{Y}_{t-h}\mid \mid_{F}^{2}\).