A Transformer-based A Multi-Horizon Quantile Recurrent Forecaster (2017, 137)

Contents

- Abstract

- Introduction

- Related Works

- Methodology

- loss function

-

architecture

-

training method

- encoder extension

- practical consideration

0. Abstract

Probabilistic Multi-step TS regression

- key 1) seq2seq

- key 2) Quantile Regression

- new training scheme : forking-seqeuences

- Multivariate

- use both “temporal & static” covariates

Test on

- 1) Amazon.com

- 2) electricity price and load

1. Introduction

Goal :

- predict \(y_{t+1}\)

- given \(y_{: t}=\left(y_{t}, \cdots, y_{0}\right)\)

Many related time-series are present!

- ex 1) dynamic historical features

- ex 2) static attributes

most of models are built on “one-step-ahead” approach

-

estimate \(\hat{y}_{t+1}\), given \(y_{: t}\)

-

called Recursive Strategy

( = Iterative = Read-outs )

-

problem : error accumulation

Direct strategy

- direclty predicts \(y_{t+k}\) given \(y_{: t}\)

- less biased / more stable / more robust

- Multi-horizon strategy

- predict \(\left(y_{t+1}, \cdots, y_{t+k}\right)\)

- avoid error accumulation

- retains efficiency by sharing parameters

Probabilistic Forecast

-

\(p\left(y_{t+k} \mid y_{: t}\right)\).

-

traditionally achieved by assuming an error distribution ( or stochastic process )

( Gaussian, on the residual series \(\epsilon_{t}=y_{t}-\hat{y}_{t}\). )

-

Quantile Regression

- predict conditional quantiles \(y_{t+k}^{(q)} \mid y_{: t}\)

- \(\mathbb{P}\left(y_{t+k} \leq y_{t+k}^{(q)} \mid y_{: t}\right)=q\).

- robust ( \(\because\) no distributional assumptions )

MQ-R(C)NN

- seq2seq framework

- generate Multi-horizion Quantile forecasts

- \(p\left(y_{t+k, i}, \cdots, y_{t+1, i} \mid y_{: t, i}, x_{: t, i}^{(h)}, x_{t:, i}^{(f)}, x_{i}^{(s)}\right)\).

- \(y_{\cdot, i}\) : \(i\) th target TS

- 1) \(x_{: t, i}^{(h)}\) : temporal covariates ( available in history )

- 2) \(x_{t:, i}^{(f)}\) : knowledge about the future

- 3) \(x_{i}^{(s)}\) : static, time-invariant features

-

each series : considered as one sample

( fed into single RNN / CNN )

- enables cross-series learning, cold-start forecasting

First work to combine RNNs & 1d-CNNs with QR or Multi-horizon forecasts

2. Related Work

[1] RNNs & CNNs

- point forecasting

[2] Cinar et al (2017)

-

attention model for seq2seq

on both UNIVARIATE & MULTIVARIATE ts

-

but, built on Recusrive Strategy

[3] Taieb and Atiya (2016)

- multi-step strategies on MLP

- Direct Multi-horizon strategy

[4] DeepAR (2017)

- probabilistic forecasting

- outputs “parameters of Negative Binomial”

- trained by maximizing likelihood & Teacher Forcing

[5] MQ-R(C)NN

- more practical than relevant Multi-horizon strategy

- more efficient training strategy

3. Method

-

loss function

-

architecture

-

training method

- encoder extension

- practical consideration

(1) loss function

Quantile Loss :

- \(L_{q}(y, \hat{y})=q(y-\hat{y})_{+}+(1-q)(\hat{y}-y)_{+}\).

- \((\cdot)_{+}=\max (0, \cdot)\).

- when \(q=0.5\) : just MAE

- \(K\) : # of horizons of forecasts

- \(Q\) : # of quantiles of interest

\(\hat{\mathbf{Y}}=\left[\hat{y}_{t+k}^{(q)}\right]_{k, q}\) :

- \(K \times Q\) matrix

- output of of parametric model \(g\left(y_{: t}, x, \theta\right)\)

Total Loss : \(\sum_{t} \sum_{q} \sum_{k} L_{q}\left(y_{t+k}, \hat{y}_{t+k}^{(q)}\right)\)

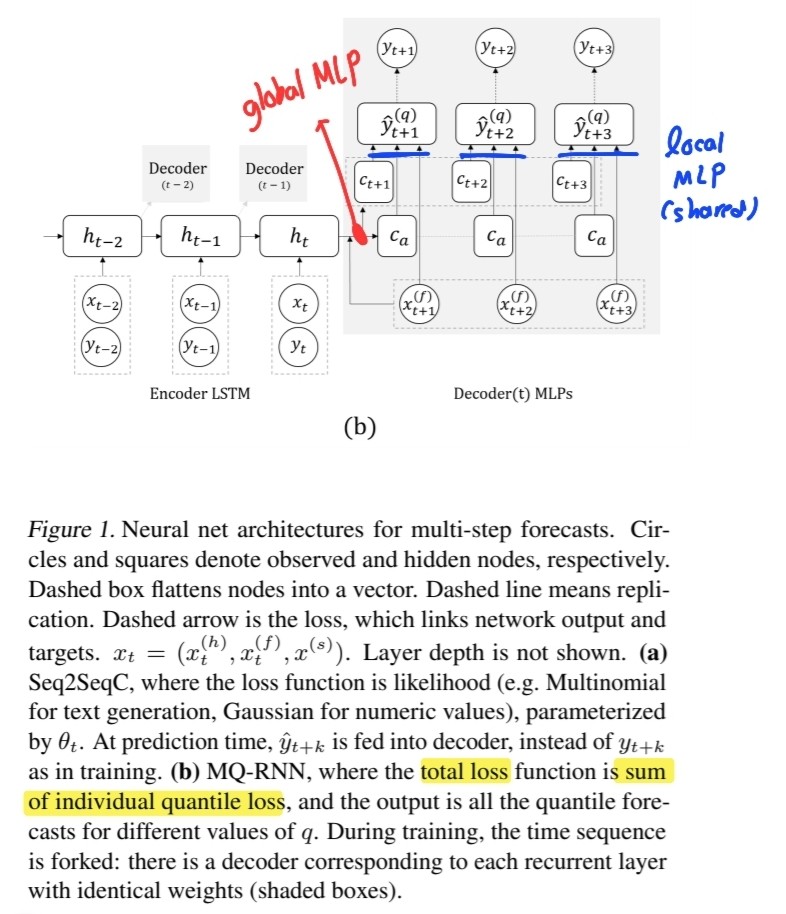

(2) architecture

- base : RNN seq2seq

- encoder : LSTM

- (recursive) deocder :2 MLP branches

- 1) (global) MLP

- 2) (local) MLP

1) (global) MLP

- \(\left(c_{t+1}, \cdots, c_{t+K}, c_{a}\right)=m_{G}\left(h_{t}, x_{t:}^{(f)}\right)\).

- input : “encoder output” & “future inputs”

- output : 2 contexts

- # 1) horizon-specific context : \(c_{t+k}\) ( for each \(K\) future points )

- # 2) horizon-agnostic context : \(c_a\)

2) (local) MLP

-

\(\left(\hat{y}_{t+k}^{\left(q_{1}\right)}, \cdots, \hat{y}_{t+k}^{\left(q_{Q}\right)}\right)=m_{L}\left(c_{t+k}, c_{a}, x_{t+k}^{(f)}\right)\).

-

applies to each specific horizon

- parameters are shared across all horizons \(k \in\{1, \cdots, K\}\)

- generate sharp & spiky forecats

- tempting to use LSTM, but unnecessary & expensive!

(3) training method

Forking-sequences training scheme

- endpoint

- where ENC & DEC exchange

- also called FCT(Forecast Creation Time)

- time step where future horizons must be generated

- mathematical expression

- 1) encoder : LSTM

- \(\forall t, h_{t}=\operatorname{encoder}\left(x_{: t}, y_{: t}\right)\).

- 2) decoder : global/local MLPs

- \(\hat{y}_{t:}^{(q)}=\operatorname{decoder}\left(h_{t}, x_{t:}^{(f)}\right)\).

- 1) encoder : LSTM

Direct strategy :

- criticized as not being able to use data between \(T-K\) & \(T\)

- thus, mask all the error terms after that point

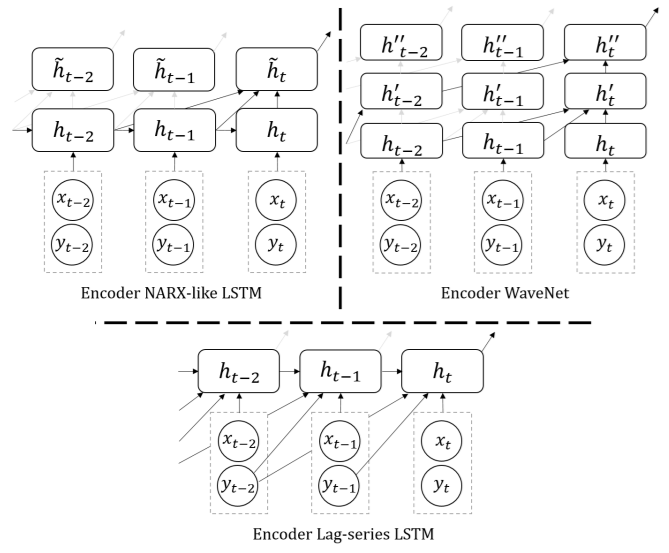

(4) encoder extension

many forecasting problems have long periodicity ( e.g 365 days)

& suffer from memory loss

NARX RNN

-

compute hidden state \(h_t\),

-

not only based on \(h_{t-1}\)

-

but also \((h_{t-2},...h_{t-D})\)

( = skip connection )

-

-

put an extra linear layer on top of LSTM to summarize them

- \(\tilde{h}_{t}=m\left(h_{t}, \cdots, h_{t-D}\right)\).

Lag-seires LSTM

- feed past series as lagged feature inputs

- \(\left(y_{t-1}, \cdots, y_{t-D}\right)\).

WaveNet

- not restricted to RNN

- WaveNet : stack of dilated causal 1d-Conv

(5) future & static features

[1] Future Features

- [1-1] seasonal features

- [1-2] event features

[2] Static Features