Sequences, Time Series and Prediction

( 참고 : coursera의 Sequences, Time Series and Prediction 강의 )

[ Week 1 ] Sequence and Predictions

- Import Packages

- Plotting Function,

plot_series - TS with trend

- TS with seasonality

- TS with trend + seasonality

- TS with trend+seasonality+noise

- Preparing Forecast

- Forecast

1. Import Packages

import numpy as np

import matplotlib.pyplot as plt

import tensorflow as tf

from tensorflow import keras

print(tf.__version__)

2.6.0

2. Plotting Function, plot_series

def plot_series(time, series, format="-", start=0, end=None, label=None):

plt.plot(time[start:end], series[start:end], format, label=label)

plt.xlabel("Time")

plt.ylabel("Value")

if label:

plt.legend(fontsize=14)

plt.grid(True)

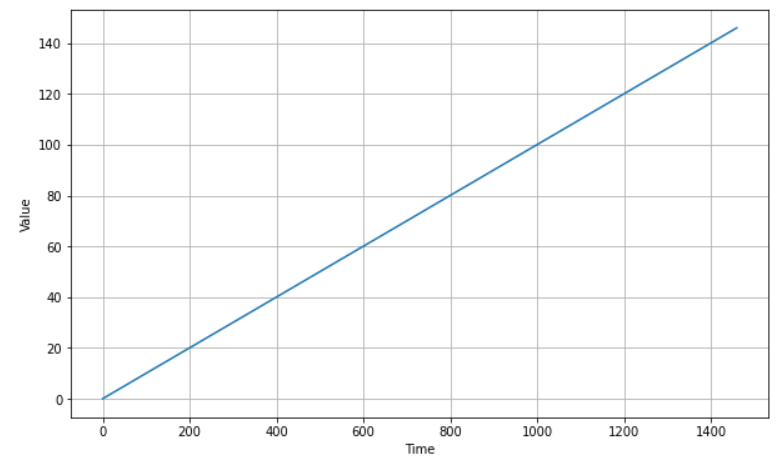

3. TS with trend

(1) trend

def trend(time, slope=0):

return slope * time

(2) make synthetic dataset

time = np.arange(4 * 365 + 1)

series = trend(time, 0.1)

print(time)

print(series)

[ 0 1 2 ... 1458 1459 1460]

[0.000e+00 1.000e-01 2.000e-01 ... 1.458e+02 1.459e+02 1.460e+02]

(3) plotting

plt.figure(figsize=(10, 6))

plot_series(time, series)

plt.show()

4. TS with seasonality

(1) seasonal_pattern

( 임의의 seasonal pattern을 만들어내는 함수 )

def seasonal_pattern(season_time):

return np.where(season_time < 0.4,

np.cos(season_time * 2 * np.pi), # if TRUE

1 / np.exp(3 * season_time)) # if FALSE

example= (time % 365) / 365

plt.plot(example)

plt.plot(seasonal_pattern(example))

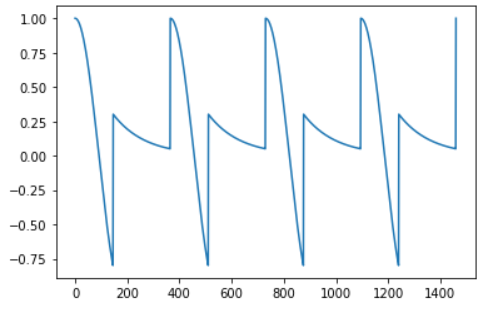

(2) seasonality

def seasonality(time, period, amplitude=1, phase=0):

season_time = ((time + phase) % period) / period

season_pattern = seasonal_pattern(season_time)

return amplitude * season_pattern

진폭 ( scale )을 40배로!

365일마다 반복되는 seasonality

amplitude = 40

period=365

series = seasonality(time, period=period, amplitude=amplitude)

시각화

plt.figure(figsize=(10, 6))

plot_series(time, series)

plt.show()

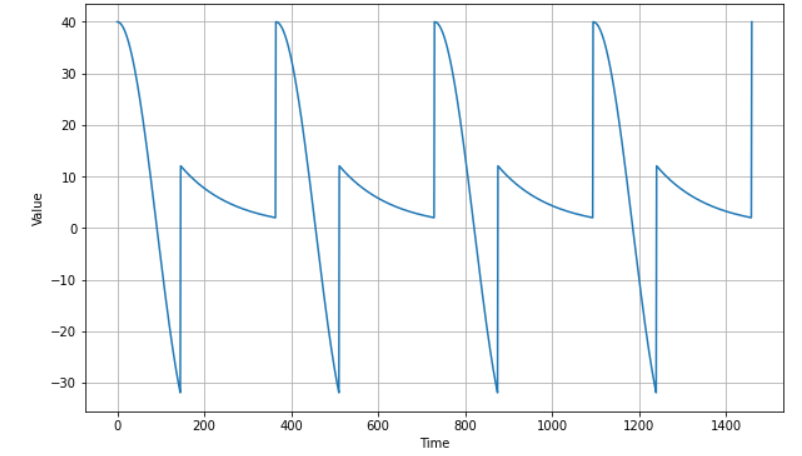

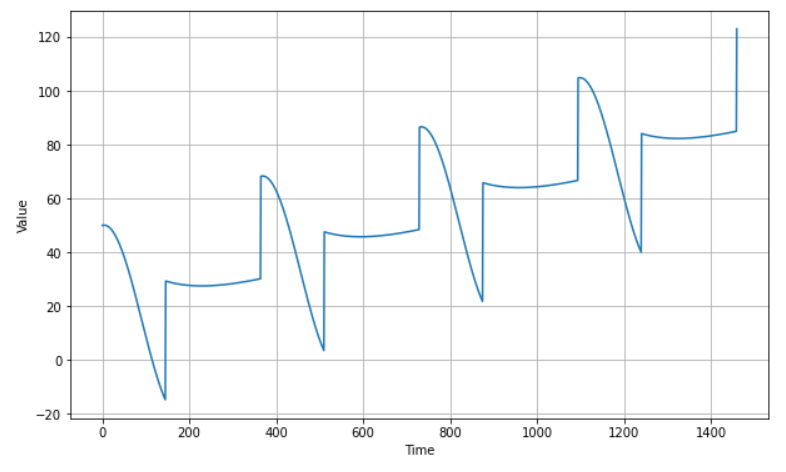

5. TS with trend + seasonality

slope = 0.05

baseline=10

series = baseline + trend(time, slope) + seasonality(time, period=period, amplitude=amplitude)

plt.figure(figsize=(10, 6))

plot_series(time, series)

plt.show()

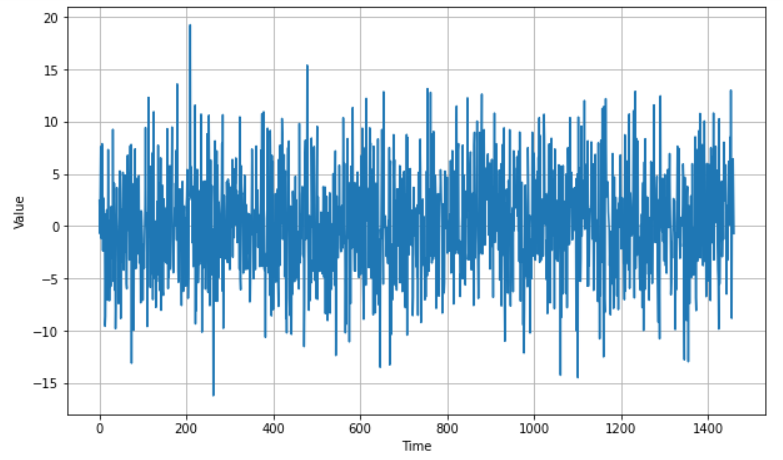

6. TS with trend+seasonality+noise

White Noise를 생성하는 함수

def white_noise(time, noise_level=1, seed=None):

rnd = np.random.RandomState(seed)

return rnd.randn(len(time)) * noise_level

Noise 수준 : \(5 \times N(0,1)\)

noise_level = 5

noise = white_noise(time, noise_level, seed=42)

plt.figure(figsize=(10, 6))

plot_series(time, noise)

plt.show()

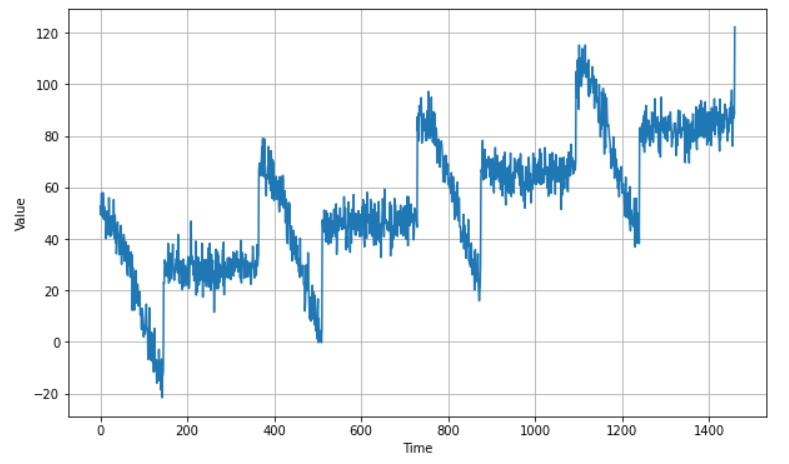

위에서 생성한 time series에 noise를 더한 뒤 시각화

series += noise

plt.figure(figsize=(10, 6))

plot_series(time, series)

plt.show()

7. Preparing Forecast

(1) make synthetic dataset

hyperparameters

baseline = 10

amplitude = 40

slope = 0.05

noise_level = 5

trend + seasonality + noise

time = np.arange(4 * 365 + 1, dtype="float32")

series = baseline + trend(time, slope) + seasonality(time, period=365, amplitude=amplitude)

series += noise(time, noise_level, seed=42)

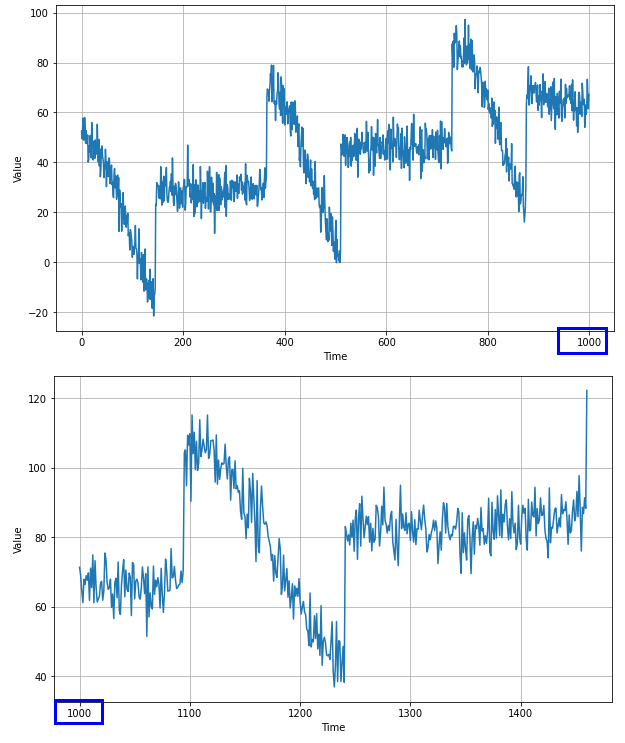

(2) Train & Validation Split

- ~1000개 : train

- 1001개~ : validation

split_time = 1000

time_train = time[:split_time]

x_train = series[:split_time]

time_valid = time[split_time:]

x_valid = series[split_time:]

Univariate Time Series

print(time_train.shape)

print(x_train.shape) # Univariate

print(time_valid.shape)

print(x_valid.shape) # Univariate

(1000,)

(1000,)

(461,)

(461,)

plt.figure(figsize=(10, 6))

plot_series(time_train, x_train)

plt.show()

plt.figure(figsize=(10, 6))

plot_series(time_valid, x_valid)

plt.show()

8. Forecast

(1) Naive Forecast

이전 시점의 값을 다음 시점의 예측값으로 사용

naive_forecast = series[split_time - 1:-1]

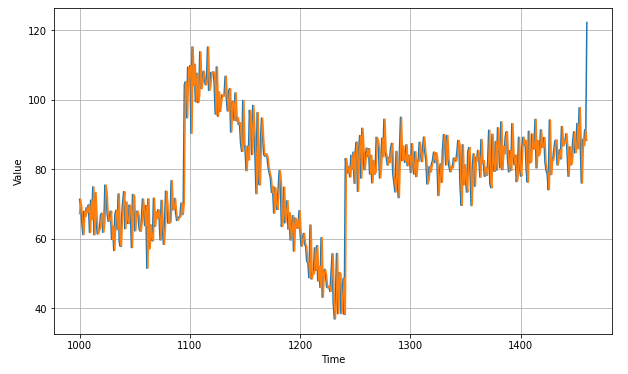

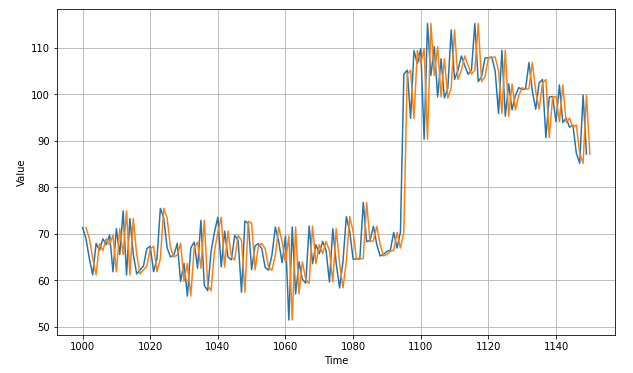

Validation 데이터의 예측 결과

- 전체 (time 1000~1461)

- 확대 (time 1000~1150)

# 전체

plt.figure(figsize=(10, 6))

plot_series(time_valid, x_valid)

plot_series(time_valid, naive_forecast)

# 확대

plt.figure(figsize=(10, 6))

plot_series(time_valid, x_valid, start=0, end=150)

plot_series(time_valid, naive_forecast, start=1, end=151)

예측 성능 (MSE & MAE)

print(keras.metrics.mean_squared_error(x_valid, naive_forecast).numpy())

print(keras.metrics.mean_absolute_error(x_valid, naive_forecast).numpy())

61.827534

5.937908

(2) Moving Average (MA)

window size를 지정해줘야

- “window size=1의 MA” = “naive forecast”

def moving_average_forecast(series, window_size):

forecast = []

for time in range(len(series) - window_size):

forecast.append(series[time:time + window_size].mean())

return np.array(forecast)

length 확인하기

series: 전체 데이터셋…train&valid ( = 0~1461 )moving_average_forecast(series, 30): 예측 결과…train&valid ( = 0~(1461-1430) )moving_avg: 예측 결과…valid ( = 1000 ~ 1461 )

moving_avg = moving_average_forecast(series, 30)[split_time - 30:]

print(len(series))

print(len(moving_average_forecast(series, 30)))

print(moving_avg)

1461

1431

461

예측 성능 (MSE & MAE)

print(keras.metrics.mean_squared_error(x_valid, moving_avg).numpy())

print(keras.metrics.mean_absolute_error(x_valid, moving_avg).numpy())

106.674576

7.142419

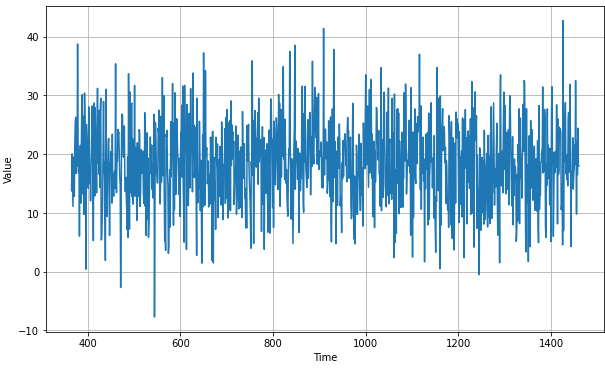

(3) 차분 후 MA

1년(=365일)전 값을 빼줌

- ex) 2021년 7월 29 값 - 2020년 7월 29일 값

lag=365

diff_series = (series[lag:] - series[:-lag])

diff_time = time[lag:]

1461일-365일 = 1096일

len(diff_series),len(diff_time)

(1096, 1096)

plt.figure(figsize=(10, 6))

plot_series(diff_time, diff_series)

plt.show()

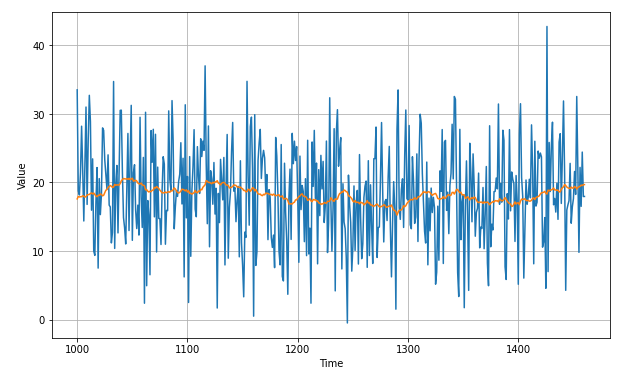

window_size=50

lag=365

diff_moving_avg = moving_average_forecast(diff_series, 50)[split_time - lag - window_size:]

plt.figure(figsize=(10, 6))

plot_series(time_valid, diff_series[split_time - lag:])

plot_series(time_valid, diff_moving_avg)

plt.show()

365일 전 값들을 다시 더해줘야!

diff_moving_avg_plus_past = series[split_time - lag:-lag] + diff_moving_avg

plt.figure(figsize=(10, 6))

plot_series(time_valid, x_valid)

plot_series(time_valid, diff_moving_avg_plus_past)

plt.show()

예측 성능 (MSE & MAE)

print(keras.metrics.mean_squared_error(x_valid, diff_moving_avg_plus_past).numpy())

print(keras.metrics.mean_absolute_error(x_valid, diff_moving_avg_plus_past).numpy())

52.973663

5.839311

(4) 차분 후 MA + smoothing

diff_moving_avg = moving_average_forecast(diff_series, 50)[split_time - lag - window_size:]

# BEFORE (smoothing X)

diff_moving_avg_plus_past = series[split_time - 365:-365] + diff_moving_avg

# AFTER (smoothing O)

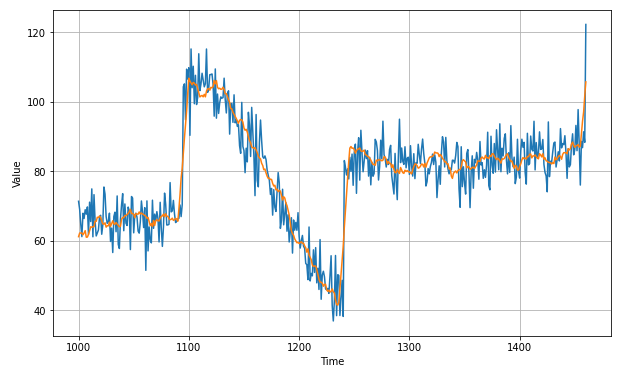

diff_moving_avg_plus_smooth_past = moving_average_forecast(series[split_time - (lag+5):-(lag-5)], 10) + diff_moving_avg

plt.figure(figsize=(10, 6))

plot_series(time_valid, x_valid)

plot_series(time_valid, diff_moving_avg_plus_smooth_past)

plt.show()

예측 성능 (MSE & MAE)

print(keras.metrics.mean_squared_error(x_valid, diff_moving_avg_plus_smooth_past).numpy())

print(keras.metrics.mean_absolute_error(x_valid, diff_moving_avg_plus_smooth_past).numpy())

33.452263

4.569442