Univariate 2. 일반 선형확률 과정 ( General Linear Process ) (2)

“시계열 데이터 = 가우시안 백색잡음의 현재값과 과거값의 선형조합”

\(Y_t = \epsilon_t + \psi_1\epsilon_{t-1} + \psi_2\epsilon_{t-2} + \cdots\).

where \(\epsilon_i \sim i.i.d.~WN(0, \sigma_{\epsilon_i}^2)~and~\displaystyle \sum_{i=1}^{\infty}\psi_i^2 < \infty\).

세부 알고리즘:

- WN(White Noise)

- MA(Moving Average)

- AR(Auto-Regressive)

- ARMA(Auto-Regressive Moving Average)

- ARMAX(ARMA with eXogenous variables)

4. ARMA(Auto-Regressive Moving Average)

\(ARMA(p,q)\): 알고리즘의 차수(\(p,q\))가 유한한 \(AR(p)\)와 \(MA(q)\)의 Linear Combination”

( 즉, \(Y_t\)는 \(Y_t\) & \(\epsilon_t\)의 차분들 (lagged variables)의 조합으로 생성 )

- \(\begin{align*} where~\epsilon_i \sim i.i.d.~WN(0, \sigma_{\epsilon_i}^2)~and~\displaystyle \sum_{i=1}^{\infty}\phi_i^2 < \infty, \displaystyle \sum_{i=1}^{\infty}\theta_i^2 < \infty \end{align*}\).

위 식을 다시 정리하면…

\[\phi(L)Y_t = \theta(L)\epsilon_t\]\(\begin{align*}

Y_t &= \dfrac{\theta(L)}{\phi(L)}\epsilon_t \\

&= \psi(L)\epsilon_t \text{ where } \psi(L) = \dfrac{\theta(L)}{\phi(L)} \\

&= (1 + \psi_1L + \psi_2L^2 + \cdots)\epsilon_t \\

&= \epsilon_t + \psi_1\epsilon_{t-1} + \psi_2\epsilon_{t-2} + \cdots\end{align*}\)

where

Autocorrelation(“Yule-Walker Equation”)

- \(\rho_i = \phi_1 \rho_{i-1} + \cdots + \phi_p \rho_{i-p}\).

[ Example ]

import pandas as pd

import numpy as np

import statsmodels

import statsmodels.api as sm

import matplotlib.pyplot as plt

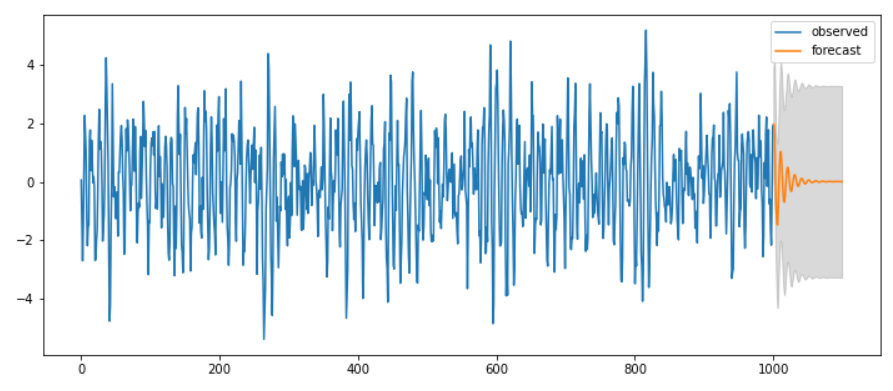

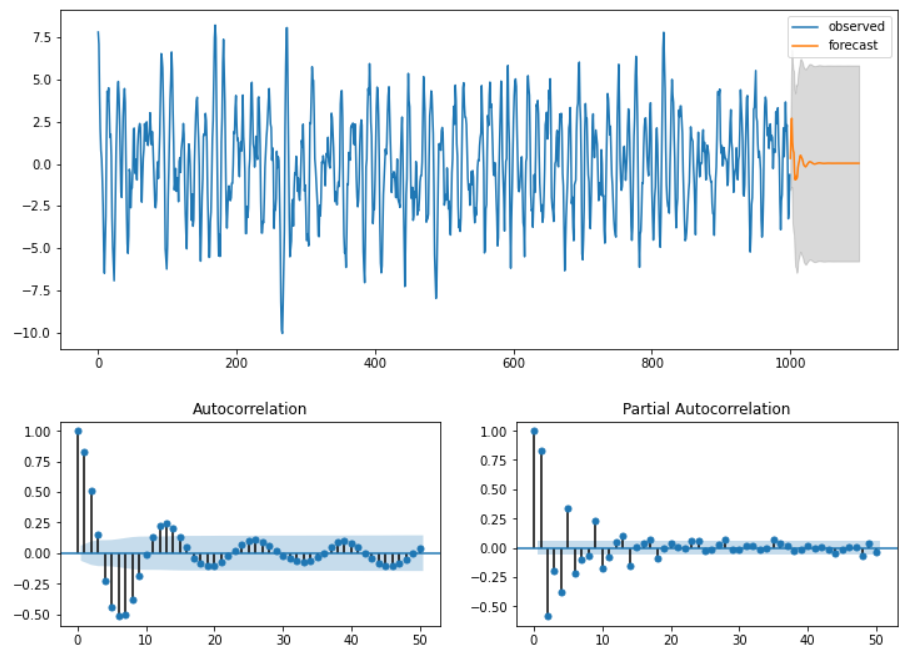

Ex 1) ARMA(2,0) = AR(2)

[Step 1] Setting

ar_params = np.array([0.75, -0.25])

ma_params = np.array([])

ar, ma = np.r_[1, -ar_params], np.r_[1, ma_params]

ar_order, ma_order = len(ar)-1, len(ma)-1

print(ar)

print(ma)

print(ar_order)

print(ma_order)

#----------------------------------------------------#

[ 1. -0.75 0.25]

[1.]

2

0

[Step 2] Simulate data from an ARMA.

statsmodels.tsa.arima_process.arma_generate_sample

y = statsmodels.tsa.arima_process.arma_generate_sample(ar, ma, nsample=1000, burnin=500)

y_df =pd.DataFrame(y)

[Step 3] Fit Model

statsmodels.tsa.arima_model.ARMAtrend='c': constant 추가

fit = statsmodels.tsa.arima_model.ARMA(y, (ar_order,ma_order)).fit(trend='c', disp=0)

[Step 4] Forecast Result

ahead = 100

pred_ts_point = fit.forecast(steps=ahead)[0]

pred_ts_interval = fit.forecast(steps=ahead)[2]

print(pred_ts_point.shape)

print(pred_ts_interval.shape) # default : alpha=0.05

print(pred_ts_point[0]==np.mean(pred_ts_interval[0]))

#----------------------------------------------------#

(100,)

(100, 2)

True

forecast_index :

-

예측하려는 대상의 time

-

1000 ~ 1000+ahead(=1100)

forecast_index = [i for i in range(y_df.index.max()+1,y_df.index.max()+ahead+1)]

pred_point_df=pd.DataFrame(pred_ts_point, index=forecast_index)

pred_interval_df = pd.DataFrame(pred_ts_interval, index=forecast_index)

print(pred_point_df.head())

print(pred_interval_df.head())

#----------------------------------------------------#

0

1000 1.971779

1001 1.940186

1002 1.492918

1003 0.058082

1004 -0.935687

0 1

1000 0.093410 3.850149

1001 -0.404395 4.284767

1002 -0.921029 3.906864

1003 -2.385855 2.502019

1004 -3.433020 1.561645

[Step 5] Result

main_plot = y_df.plot(figsize=(12,5))

pred_point_df.plot(label='forecast', ax=main_plot)

main_plot.fill_between(pred_interval_df.index,

pred_interval_df.iloc[:,0],pred_interval_df.iloc[:,1],

color='k', alpha=0.15)

plt.legend(['observed', 'forecast'])

display(fit.summary2())

| Model: | ARMA | BIC: | 2796.4388 |

|---|---|---|---|

| Dependent Variable: | y | Log-Likelihood: | -1377.5 |

| Date: | 2021-09-01 12:20 | Scale: | 1.0000 |

| No. Observations: | 1000 | Method: | css-mle |

| Df Model: | 5 | Sample: | 0 |

| Df Residuals: | 995 | 0 | |

| Converged: | 1.0000 | S.D. of innovations: | 0.958 |

| No. Iterations: | 12.0000 | HQIC: | 2778.184 |

| AIC: | 2766.9923 |

| Coef. | Std.Err. | t | P>|t| | [0.025 | 0.975] | |

|---|---|---|---|---|---|---|

| const | 0.0093 | 0.0374 | 0.2500 | 0.8026 | -0.0639 | 0.0826 |

| ar.L1.y | 0.7470 | 0.0279 | 26.7627 | 0.0000 | 0.6923 | 0.8017 |

| ar.L2.y | -0.2521 | 0.0362 | -6.9600 | 0.0000 | -0.3231 | -0.1811 |

| ar.L3.y | 0.1631 | 0.0362 | 4.4995 | 0.0000 | 0.0920 | 0.2341 |

| ar.L4.y | -0.4699 | 0.0279 | -16.8256 | 0.0000 | -0.5247 | -0.4152 |

| Real | Imaginary | Modulus | Frequency | |

|---|---|---|---|---|

| AR.1 | 0.8756 | -0.6261 | 1.0764 | -0.0988 |

| AR.2 | 0.8756 | 0.6261 | 1.0764 | 0.0988 |

| AR.3 | -0.7021 | -1.1592 | 1.3553 | -0.3367 |

| AR.4 | -0.7021 | 1.1592 | 1.3553 | 0.3367 |

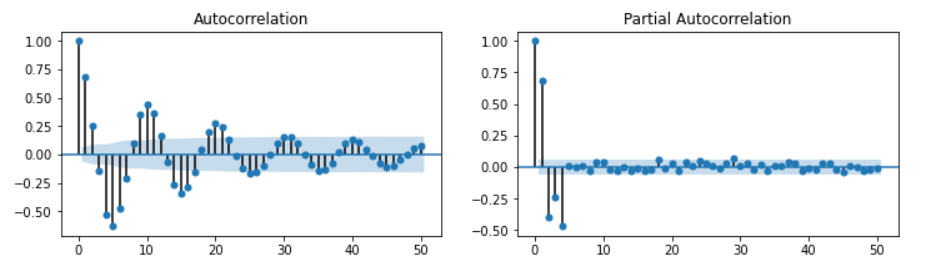

plt.figure(figsize=(12,3))

statsmodels.graphics.tsaplots.plot_acf(y, lags=50, zero=True, use_vlines=True,

alpha=0.05, ax=plt.subplot(121))

statsmodels.graphics.tsaplots.plot_pacf(y, lags=50, zero=True, use_vlines=True,

alpha=0.05, ax=plt.subplot(122))

plt.show()

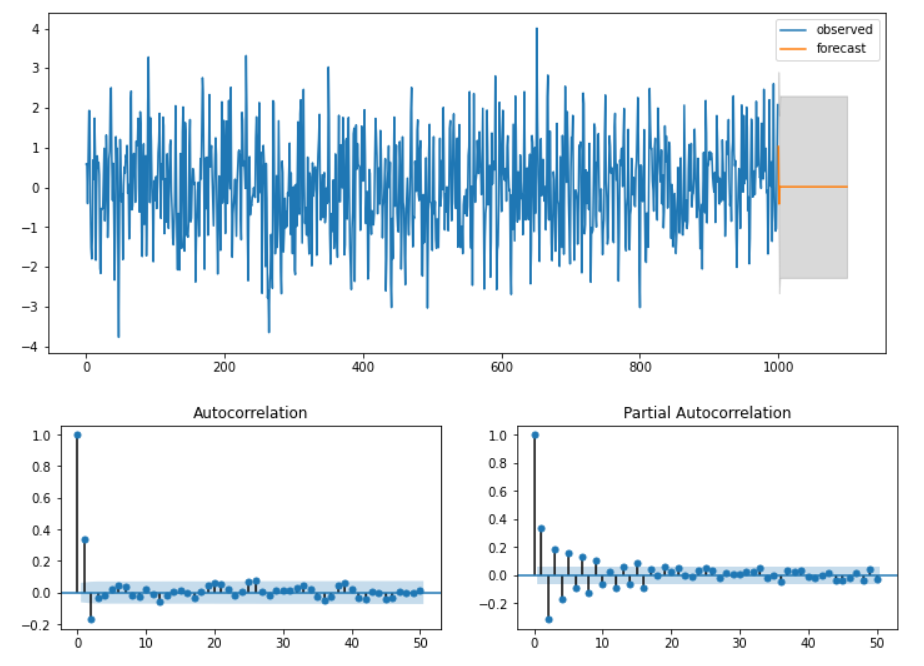

Ex 2) ARMA(0,2) = MA(2)

ar_params = np.array([])

ma_params = np.array([0.65, -0.25])

| Model: | ARMA | BIC: | 2783.1398 |

|---|---|---|---|

| Dependent Variable: | y | Log-Likelihood: | -1377.8 |

| Date: | 2020-09-29 23:34 | Scale: | 1.0000 |

| No. Observations: | 1000 | Method: | css-mle |

| Df Model: | 3 | Sample: | 0 |

| Df Residuals: | 997 | 0 | |

| Converged: | 1.0000 | S.D. of innovations: | 0.959 |

| No. Iterations: | 8.0000 | HQIC: | 2770.970 |

| AIC: | 2763.5088 |

| Coef. | Std.Err. | t | P>|t| | [0.025 | 0.975] | |

|---|---|---|---|---|---|---|

| const | 0.0130 | 0.0425 | 0.3053 | 0.7602 | -0.0703 | 0.0962 |

| ma.L1.y | 0.6501 | 0.0310 | 20.9416 | 0.0000 | 0.5892 | 0.7109 |

| ma.L2.y | -0.2487 | 0.0307 | -8.0906 | 0.0000 | -0.3090 | -0.1885 |

| Real | Imaginary | Modulus | Frequency | |

|---|---|---|---|---|

| MA.1 | -1.0865 | 0.0000 | 1.0865 | 0.5000 |

| MA.2 | 3.7001 | 0.0000 | 3.7001 | 0.0000 |

Ex 3) ARMA(1,1)

ar_params = np.array([0.75])

ma_params = np.array([0.65])

| Model: | ARMA | BIC: | 2783.7601 |

|---|---|---|---|

| Dependent Variable: | y | Log-Likelihood: | -1378.1 |

| Date: | 2020-07-31 22:45 | Scale: | 1.0000 |

| No. Observations: | 1000 | Method: | css-mle |

| Df Model: | 3 | Sample: | 0 |

| Df Residuals: | 997 | 0 | |

| Converged: | 1.0000 | S.D. of innovations: | 0.959 |

| No. Iterations: | 9.0000 | HQIC: | 2771.590 |

| AIC: | 2764.1291 |

| Coef. | Std.Err. | t | P>|t| | [0.025 | 0.975] | |

|---|---|---|---|---|---|---|

| const | 0.0641 | 0.1970 | 0.3252 | 0.7450 | -0.3220 | 0.4501 |

| ar.L1.y | 0.7465 | 0.0224 | 33.3502 | 0.0000 | 0.7027 | 0.7904 |

| ma.L1.y | 0.6519 | 0.0261 | 24.9637 | 0.0000 | 0.6007 | 0.7031 |

| Real | Imaginary | Modulus | Frequency | |

|---|---|---|---|---|

| AR.1 | 1.3395 | 0.0000 | 1.3395 | 0.0000 |

| MA.1 | -1.5340 | 0.0000 | 1.5340 | 0.5000 |

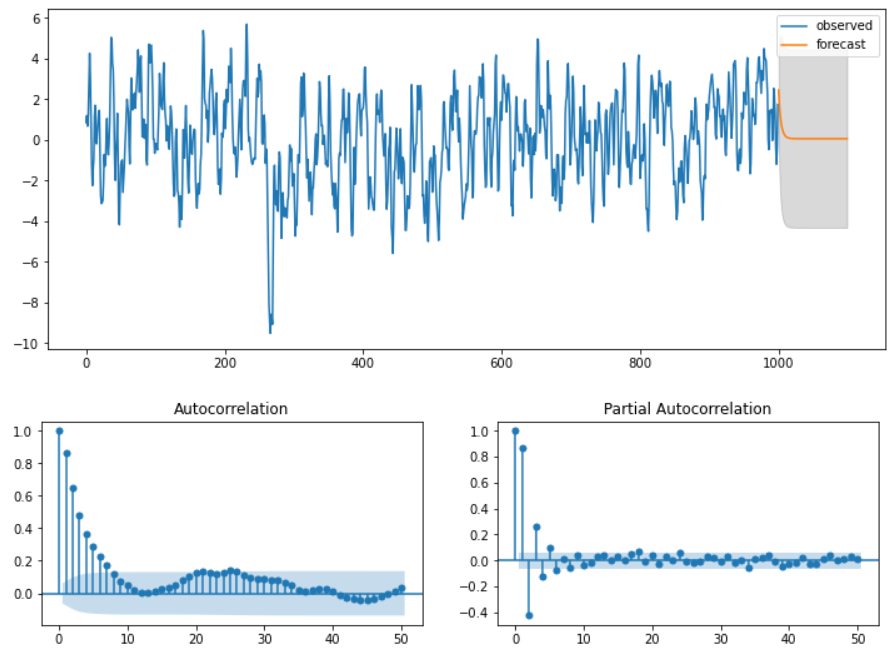

Ex 4) ARMA(5,5)

ar_params = np.array([0.75, -0.25, 0.5, -0.5, -0.1])

ma_params = np.array([0.65, 0.5, 0.2, -0.5, -0.1])

| Model: | ARMA | BIC: | 2844.4865 |

|---|---|---|---|

| Dependent Variable: | y | Log-Likelihood: | -1380.8 |

| Date: | 2020-09-29 23:41 | Scale: | 1.0000 |

| No. Observations: | 1000 | Method: | css-mle |

| Df Model: | 11 | Sample: | 0 |

| Df Residuals: | 989 | 0 | |

| Converged: | 1.0000 | S.D. of innovations: | 0.959 |

| No. Iterations: | 54.0000 | HQIC: | 2807.977 |

| AIC: | 2785.5934 |

| Coef. | Std.Err. | t | P>|t| | [0.025 | 0.975] | |

|---|---|---|---|---|---|---|

| const | 0.0308 | 0.0864 | 0.3569 | 0.7212 | -0.1386 | 0.2003 |

| ar.L1.y | 1.3387 | 0.4949 | 2.7049 | 0.0068 | 0.3687 | 2.3087 |

| ar.L2.y | -0.7833 | 0.4780 | -1.6387 | 0.1013 | -1.7202 | 0.1536 |

| ar.L3.y | 0.7138 | 0.2246 | 3.1786 | 0.0015 | 0.2737 | 1.1540 |

| ar.L4.y | -0.7757 | 0.2729 | -2.8428 | 0.0045 | -1.3106 | -0.2409 |

| ar.L5.y | 0.2339 | 0.2687 | 0.8705 | 0.3840 | -0.2927 | 0.7604 |

| ma.L1.y | 0.0678 | 0.4967 | 0.1366 | 0.8914 | -0.9057 | 1.0413 |

| ma.L2.y | 0.2093 | 0.2164 | 0.9674 | 0.3334 | -0.2148 | 0.6334 |

| ma.L3.y | -0.0514 | 0.1982 | -0.2592 | 0.7955 | -0.4398 | 0.3371 |

| ma.L4.y | -0.6159 | 0.0713 | -8.6358 | 0.0000 | -0.7557 | -0.4762 |

| ma.L5.y | 0.1658 | 0.2752 | 0.6026 | 0.5467 | -0.3735 | 0.7052 |

| Real | Imaginary | Modulus | Frequency | |

|---|---|---|---|---|

| AR.1 | -0.4994 | -1.1024 | 1.2103 | -0.3177 |

| AR.2 | -0.4994 | 1.1024 | 1.2103 | 0.3177 |

| AR.3 | 1.0036 | -0.5072 | 1.1245 | -0.0745 |

| AR.4 | 1.0036 | 0.5072 | 1.1245 | 0.0745 |

| AR.5 | 2.3086 | -0.0000 | 2.3086 | -0.0000 |

| MA.1 | -1.1194 | -0.0000 | 1.1194 | -0.5000 |

| MA.2 | -0.0971 | -1.0335 | 1.0381 | -0.2649 |

| MA.3 | -0.0971 | 1.0335 | 1.0381 | 0.2649 |

| MA.4 | 1.3648 | -0.0000 | 1.3648 | -0.0000 |

| MA.5 | 3.6628 | -0.0000 | 3.6628 | -0.0000 |

모형 차수결정 정리

- 예측하기 이전에, parameter ( = p, q ) 에 따라 모형이 어떠한 모습을 띌 지 예상해봐야!

- \(p\), \(q\) 파라미터 추론(by ACF and PACF):

- 정상성 형태 변환

- ACF & PACF 도식화

| 자기회귀: \(AR(p)\) | 이동평균: \(MA(q)\) | 자기회귀이동평균: \(ARMA(p,q)\) | |

|---|---|---|---|

| \(ACF\) | 지수적 감소, 진동하는 sine 형태 | \(q+1\) 차항부터 절단모양(0수렴) | \(q+1\) 차항부터 지수적 감소 혹은 진동하는 sine 형태 |

| \(PACF\) | \(p+1\) 차항부터 절단모양(0수렴) | 지수적 감소, 진동하는 sine 형태 | \(p+1\) 차항부터 지수적 감소 혹은 진동하는 sine 형태 |

5. ARMAX ( ARMA with eXogenous)

ARMA에 \(\beta X\) 가 추가된 형태

ARMA 식

- \(Y_t = \phi_1Y_{t-1} + \phi_2Y_{t-2} + \cdots + \phi_pY_{t-p} + \theta_1\epsilon_{t-1} + \theta_2\epsilon_{t-2} + \cdots + \theta_q\epsilon_{t-q} + \epsilon_t\).

ARMAX 식

- \(Y_t = \phi_1Y_{t-1} + \phi_2Y_{t-2} + \cdots + \phi_pY_{t-p} + \theta_1\epsilon_{t-1} + \theta_2\epsilon_{t-2} + \cdots + \theta_q\epsilon_{t-q} + \epsilon_t + \beta X\).

[ Example ]

Seasonal ARMAX : sm.tsa.SARIMAX

fit = sm.tsa.SARIMAX(raw_using.consump, exog=raw_using.m2,

order=(1,0,0), seasonal_order=(1,0,1,4)).fit()